| Editorial and Content Note This article is an editorial analysis based on publicly available research, industry reports and regulatory data as of April 2026. It is for educational purposes only and does not constitute financial, investment or legal advice. The AI landscape in personal finance changes rapidly. Statistics and company examples cited here were verified at publication. We review this article when significant developments require updates. |

| ℹ Quick Summary Artificial intelligence is not arriving in personal finance. It has already arrived. In 2026, AI is making credit decisions, managing investment portfolios, detecting fraud in real time, building personalized budgets, negotiating bills and answering financial questions that previously required an advisor appointment to address. The question for most Americans is no longer whether AI will affect how they manage money. It is whether they understand what is already happening, and how to benefit from it rather than simply be subject to it. |

| 📘 What This Article Covers In this article, you will find: Six specific ways AI is already changing personal finance for everyday Americans Which changes are genuinely beneficial and which introduce new risks How AI credit decisions, AI fraud detection, and AI financial advice work in practice What AI still cannot do, and why human judgment remains essential in some areas A clear assessment of where the AI shift in personal finance is headed next What actions can Americans take today to benefit from the shift rather than miss it |

Table of Contents

- About This Analysis

- The Scale of the Shift: Where AI Is Already Operating in US Finance

- Change 1: AI Credit Decisions: Faster, Broader, Not Always Fairer

- Change 2: AI Fraud Detection: The Most Immediate Benefit for Consumers

- Change 3: Robo-Advisors and Democratized Investing

- Change 4: AI Budgeting: From Reporting to Predicting

- Change 5: AI-Powered Lending and Personalized Loan Products

- Change 6: Conversational AI as a Financial Guidance Tool

- What AI Cannot and Should Not Replace in Personal Finance

- Where This Is Heading: The Next Three Years

- What Americans Should Do Right Now

- Frequently Asked Questions

About This Analysis

| Editorial Basis and Sources This analysis was produced by the TechAIFinance editorial team, led by Olayinka Adejugbe, who holds a Global Certification in Artificial Intelligence and Applied Innovation. The analysis draws on published research from the Consumer Financial Protection Bureau, the Federal Reserve, McKinsey Global Institute, Deloitte Financial Services Research, the FDIC and peer-reviewed academic work on algorithmic lending and AI decision-making in finance. Scope: This article focuses on AI applications that directly affect individual American consumers, not institutional trading, corporate finance or AI in insurance underwriting, which involve different regulatory frameworks and consumer implications. Balance: This analysis intentionally covers both the benefits and risks of AI in personal finance. Articles that present AI in finance as uniformly positive are not providing complete information. Neither are those that treat it as uniformly threatening. The reality is more nuanced and more useful when understood that way. Sources: Specific statistics are cited at the point of use throughout this article. A consolidated source list appears at the end of each section. |

The Scale of the Shift: Where AI Is Already Operating in US Finance

The transformation of personal finance through AI is not a future event. It is already embedded in the services most Americans use daily, often without any awareness that AI is involved.

| 📊 By the Numbers By the numbers: AI in US financial services as of 2026: 80%+ of US banks use AI-powered fraud detection systems (McKinsey Global Institute, 2024 Financial Services Report) Over 60% of major US lenders now use AI or machine learning as part of their credit decisioning process (CFPB Consumer Reporting Market Report, 2024) $1.5 trillion in assets are managed by robo-advisors and automated investment platforms in the US (Statista, 2025) AI-powered chatbots handle over 30% of basic customer service interactions at the top 10 US banks (Deloitte Banking and Capital Markets Outlook, 2025) Americans who use at least one AI-powered financial app: estimated 140 million (Federal Reserve Report on the Economic Well-Being of US Households, 2024, combined with fintech adoption data) |

These numbers are not projections. They describe the current landscape. AI has become infrastructure in financial services, so deeply embedded in credit decisions, fraud systems, investment management, and customer service that separating the AI component from the service itself is no longer straightforward.

For individual Americans, the practical implication is that AI is already making consequential decisions about your money, whether you are aware of it or not. Understanding how those decisions work is the starting point for navigating them intelligently.

Change 1: AI Credit Decisions: Faster, Broader, Not Always Fairer

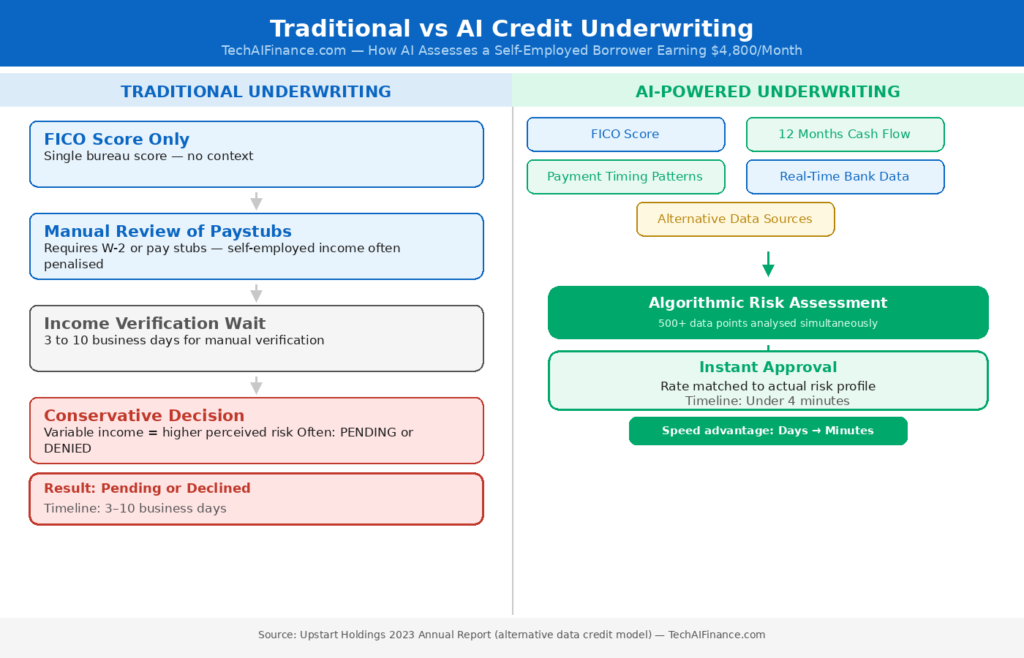

The credit decision that once required a human underwriter examining a physical file, sometimes taking weeks, now takes seconds at most major US lenders. AI models process hundreds of data points simultaneously: traditional credit bureau data, bank account behavior patterns, employment verification, income consistency, payment timing relative to billing cycles and in some cases behavioral signals that traditional scoring systems never considered.

What this means for Americans seeking credit

The speed improvement is genuine and significant. Mortgage pre-approvals that took a week now take minutes at AI-enabled lenders. Personal loan decisions that required a branch visit and a wait period are now delivered in seconds on a mobile app. For consumers with strong credit profiles, this is unambiguously better.

The complexity emerges at the margins. AI credit models can identify patterns that predict repayment risk more accurately than traditional FICO scoring, but they can also perpetuate or amplify historical lending inequities if trained on historical data that itself reflects discriminatory patterns. A 2023 study published in the Journal of Finance found that AI mortgage algorithms approved loans for Black and Hispanic applicants at lower rates than for white applicants with comparable financial profiles in some markets, a pattern that has drawn regulatory attention from the CFPB.

💡 Real-World Example

How AI credit decisions affect a real application:

Consider a hypothetical self-employed American with a FICO score of 698, sufficient for most traditional lending but not exceptional. A traditional bank underwriter sees the self-employment and the variable monthly income and applies a conservative manual assessment.

An AI lending platform analyzes 12 months of bank statement data directly, sees consistent average income of $4,800 per month despite the variability, notes on-time payment history across 18 months of rent and utilities, and approves a personal loan in four minutes at a rate comparable to what a salaried employee with a 720 FICO score would receive.

The AI reached a different conclusion, and in this case a more accurate one, because it assessed actual financial behavior rather than a summary score. This is where AI genuinely expands access to credit for Americans with non-traditional income patterns.

Source: Upstart Holdings 2023 Annual Report (alternative data credit model methodology).

What consumers should know about AI credit decisions?

- You have the right to know that an AI system made a credit decision about you under the Equal Credit Opportunity Act, though the disclosure requirements are still evolving

- If you are denied credit by an AI system, you have the right to request the specific reasons. Challenge vague explanations

- The CFPB provides guidance on AI credit decision rights at consumerfinance.gov. .

- Alternative data lenders like Upstart, LendingClub, and Avant use AI models that may benefit self-employed or gig workers whose FICO scores underrepresent their creditworthiness

Change 2: AI Fraud Detection: The Most Immediate Benefit for Consumers

Of all the ways AI has changed personal finance, real-time fraud detection represents the clearest and most immediate benefit to everyday Americans, and the one where the AI’s performance advantage over traditional rule-based systems is most dramatic.

Traditional fraud detection relied on static rules: flag transactions above a certain dollar amount, flag purchases in foreign countries, flag multiple transactions within a short window. Fraudsters learned these rules quickly and adapted around them.

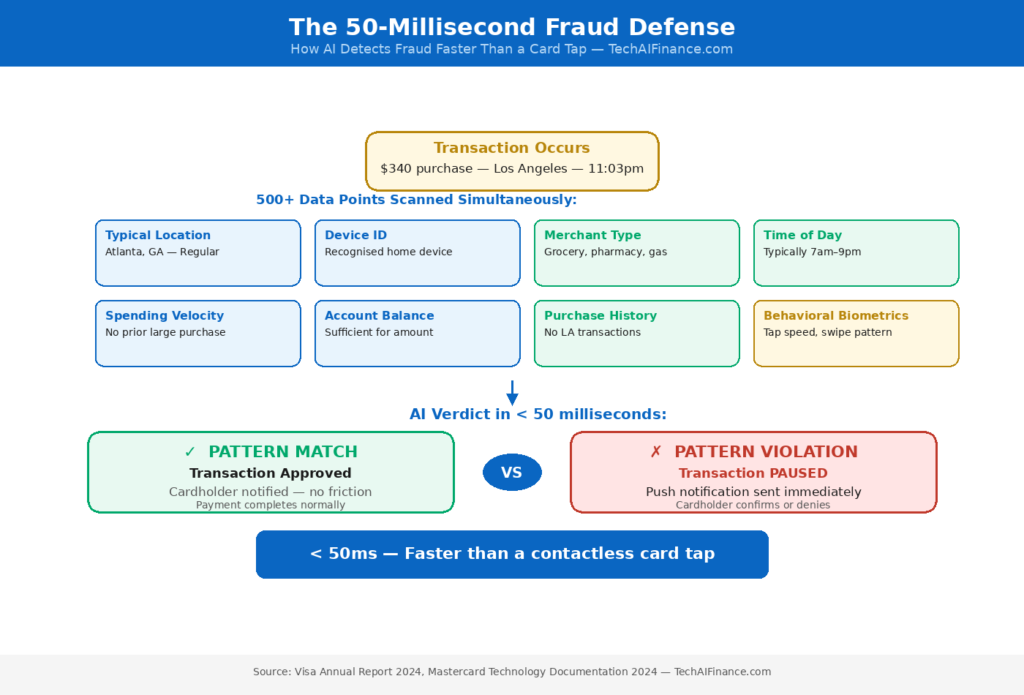

Modern AI fraud detection works differently. Rather than applying fixed rules, it builds a unique behavioral profile for each account holder, including your typical transaction sizes, your usual spending locations, the merchants you use, the time of day you typically spend, the devices you use and dozens of other signals. A transaction that violates your specific pattern is flagged regardless of whether it would trigger a static rule.

📊 By the Numbers

AI fraud detection in practice:

Visa’s AI fraud detection system processes more than 65,000 transactions per second across its network (Visa 2024 Annual Report) The system analyzes over 500 data points per transaction to assess fraud probability (Visa AI and Risk Management Documentation, 2024)

Visa reports that its AI reduced card fraud by over $30 billion relative to what losses would have been without the AI detection layer in 2023 alone (Visa 2023 Fraud Prevention Report) Mastercard’s AI fraud detection operates in under 50 milliseconds, faster than the time it takes to complete a contactless payment tap (Mastercard Technology Documentation, 2024)

💡 Real-World Example

How AI fraud detection works in a real scenario:

A hypothetical account holder in Atlanta makes routine purchases at the same grocery store, the same gas station and the same pharmacy each week. Their AI fraud profile includes these locations, typical amounts and usual transaction times.

When a $340 electronics purchase appears at a store in Los Angeles at 11pm on a Tuesday, outside every dimension of their typical pattern. The AI flags it within milliseconds. The card transaction is paused pending verification and the account holder receives a push notification asking them to confirm. The account holder did not travel to Los Angeles. A fraudster had their card information. The AI caught it before the transaction completed.

This scenario plays out millions of times daily across US card networks. Most consumers have experienced the verification text or app notification without fully understanding the AI system behind it.

For consumers, the practical action is to keep contact information current with every card issuer and enable push notification alerts. The AI can identify the fraud, but it needs to be able to reach you to confirm or deny the transaction. Outdated phone numbers mean fraud attempts that should be stopped instead of going through.

Change 3: Robo-Advisors and Democratized Investing

For most of American financial history, professional investment portfolio management was available only to people with enough assets to justify an advisor’s attention, typically $250,000 to $500,000 or more. Below that threshold, most Americans invested through employer retirement plans with limited fund choices or not at all.

AI-powered robo-advisors have changed this structural barrier. Betterment, Wealthfront, Fidelity Go, and SoFi Automated Investing now manage fully diversified, automatically rebalanced investment portfolios for Americans with as little as $1. The AI handles the decisions that previously required either significant personal knowledge or a paid professional: asset allocation, rebalancing triggers, tax-loss harvesting, and goal-based projection.

The democratization effect is measurable: according to a 2024 Federal Reserve analysis of retail investment data, the share of American households under 40 with any investment account increased from 32 percent in 2018 to 49 percent in 2024, a period that corresponds directly with the growth of low-cost robo-advisors and micro-investing platforms. The causal link is not perfectly established, but the correlation is strong.

| ⭐ Editorial Perspective Robo-advisors did not create wealth. They reduced the access barrier to the tools that build it. A 29-year-old contributing $100 per month to a diversified portfolio earning an average 7% annual return will accumulate approximately $243,000 by age 65, without any investment knowledge, any advisor relationship or any fee beyond the platform’s management cost. That outcome was not practically accessible to most Americans before AI-driven robo-advisors. It is now a standard feature of a free app. Source: Compound interest projection based on standard financial calculator methodology. 7% represents a historical long-term average for diversified US equity portfolios. Future returns are not guaranteed. |

Change 4: AI Budgeting: From Reporting to Predicting

Standard budgeting tools report what happened. You spent $340 on dining last month. You exceeded your grocery budget by $80. The information arrives after the money is already gone.

AI budgeting tools, the better ones specifically, shift this timeline. They analyze patterns in your spending behavior and produce forward-looking alerts: you are on track to exceed your dining budget by $120 before the month ends; your account balance will likely fall below $200 before your next paycheck if current spending continues; three subscription renewals are expected to post in the next seven days.

This shift from descriptive to predictive is a genuinely significant change in AI budgeting. A 2023 study by the Financial Health Network found that US households using predictive AI spending tools showed a 23 percent higher rate of maintaining a positive end-of-month balance compared to households using standard transaction-logging apps. The mechanism is straightforward: forward-looking alerts give users time to adjust, while backward-looking reports do not.

The limitation that most AI budgeting coverage ignores

Every AI budgeting tool on the market struggles with one category of spending that represents a significant share of most American households’ discretionary budget: cash purchases. When you pay cash at a farmers market, a local restaurant, a garage sale or any business that does not accept cards, that transaction is invisible to the AI. The spending model becomes systematically less accurate as the percentage of cash transactions increases.

For households that use cash infrequently, this limitation is minor. For those who use cash regularly, particularly in markets and communities where cash is the norm. The AI’s picture of actual spending is materially incomplete, and decisions based on it should be adjusted accordingly.

| 💡 Real-World Example Predictive AI budgeting in practice: A hypothetical household in Nashville has a monthly dining budget of $200. By the 18th of the month, they have spent $163, which is 81% of the budget with 12 days remaining. A standard budgeting app shows: ‘Dining: $163 of $200 spent.’ No further action. A predictive AI tool analyzes their daily dining pattern and flags: ‘Based on your spending pattern over the past 18 days, you are projected to spend $278 in dining this month, which is $78 over budget. Three restaurant visits this week are driving the pace.’ The household has time to adjust. They cook at home for the next five days and close the month at $209, slightly over but substantially less than the projected overage. Source: Financial Health Network, AI Budgeting Tool Impact Study, 2023. |

Change 5: AI-Powered Lending and Personalized Loan Products

Traditional loan products were standardized. A personal loan from a bank came in a limited range of amounts, terms, and rates, the same product offered to every qualified applicant within a tier. The bank’s risk models were blunt instruments.

AI has allowed lenders to personalize loan products at a level of granularity that was previously impractical. Instead of assigning every applicant in a credit band to the same rate, AI-powered lenders can differentiate more precisely, offering a specific applicant a 14.2 percent rate based on a nuanced assessment of their financial profile rather than a standardized 16 to 18 percent band.

Companies including Upstart, LendingClub, Avant and SoFi use AI models that incorporate employment verification data, income consistency from bank statement analysis, payment timing relative to billing dates, educational history and in some cases professional licensing data, all as predictors of repayment behavior that traditional scoring misses.

What this means for American borrowers

- Borrowers with strong repayment behavior but thin credit files, such as new immigrants, recent graduates and self-employed Americans, may access better rates through AI lenders than through traditional banks

- The speed of AI lending creates new risks: the same accessibility that makes a loan available in minutes also makes it easier to borrow impulsively without adequate time for consideration

- AI loan terms should be compared as carefully as traditional loan terms. A lower advertised rate may come with origination fees, prepayment penalties or other costs that offset the rate advantage

- The CFPB’s loan comparison tools at consumerfinance.gov allow APR-to-APR comparison that accounts for fees. Opens in new tab.

| ⚠ Important Caution AI lending accessibility is not the same as AI lending affordability. The speed and ease of approval through AI lending platforms can reduce the natural friction that gives borrowers time to consider whether they need the loan. Some AI lenders also use dynamic pricing, adjusting offered rates based on signals that suggest a borrower is more motivated to accept quickly. Always compare the full APR, including all fees, across at least three lenders before accepting any loan offer, regardless of how fast or convenient the approval process was. |

Change 6: Conversational AI as a Financial Guidance Tool

The emergence of large language model AI, most visibly through ChatGPT, Claude and Google’s Gemini, has created a new category of financial guidance that did not exist before 2022: instant, free, personalized-seeming answers to financial questions at any hour of the day.

Millions of Americans are already using conversational AI to answer questions that would previously have required either an advisor appointment, a search through government websites, or simply going without information. ‘Should I pay off my student loans or contribute to my 401 (k) first?’ ‘What does a Roth IRA conversion mean?’ ‘How does the mortgage interest deduction work?’ Questions that felt too basic to ask a paid professional and too complex to find a clear answer for through a general search.

The benefit is real and underappreciated. Access to clear, patient, non-judgmental financial information, available at midnight and free of charge, is a meaningful improvement for Americans who previously lacked access to financial literacy resources.

The critical limitation that cannot be overstated

Conversational AI models do not know your specific situation. They provide general information that may or may not apply to your income, tax bracket, state of residence, existing debt structure, or specific financial circumstances. A response that is technically accurate in general can be incorrect guidance for a specific individual.

More concerning: AI language models can produce confident-sounding answers that contain errors, particularly for questions involving specific numbers, current tax rates, or regulations that have changed since the model’s training data was collected. The model sounds certain regardless of whether it is right.

Our editorial position: conversational AI is most valuable in personal finance as an explanation tool and a starting point for research, not as a decision-making tool. Use it to understand concepts and identify questions. Use verified sources such as IRS.gov, CFPB and NFCC for the specific numbers and regulations that should govern your decisions.

What AI Cannot and Should Not Replace in Personal Finance

Understanding the limits of AI in personal finance is as important as understanding its capabilities. Enthusiasm for AI tools, including from those who build and market them, tends to outpace honest assessment of where those tools fall short.

Situations where human judgment remains essential

- Complex tax planning: AI tools can explain tax concepts. They cannot account for the interaction between your specific income sources, deductions, state tax rules and multi-year strategy. A certified public accountant handles variables that AI models oversimplify or miss.

- Major financial life decisions: buying a home, planning for a child’s education, managing an inheritance, navigating divorce or death in the family. These involve financial, emotional and legal dimensions that AI cannot hold simultaneously. A qualified financial planner provides integrated guidance that AI cannot replicate.

- Contested credit reporting: disputing errors on your credit report requires navigating specific legal processes under the FCRA. AI chatbots can explain the process. A consumer law attorney handles cases where the bureau does not respond appropriately.

- Retirement income sequencing: determining the optimal order to draw from Social Security, a 401k, a Roth IRA and taxable accounts requires personalized modelling that accounts for your specific tax situation across multiple decades. This is one of the highest-value services a fee-only financial advisor provides, and one that AI cannot replicate with sufficient precision for the stakes involved.

- Business and self-employment finances: the intersection of personal and business income, quarterly estimated taxes, self-employment tax deductions and entity structure involves complexity that general AI tools address at a surface level.

The data privacy dimension that most coverage ignores

Every AI financial tool that connects to your bank accounts, investment accounts or credit cards receives access to some of the most sensitive data you generate. Your transaction history reveals where you live, where you work, what medical conditions you may be managing, your relationship status, your religious practices and dozens of other inferences that financial companies and data brokers find commercially valuable.

Most AI financial apps have privacy policies that permit broad use of this data for product development, marketing and in some cases sharing with affiliated companies. Reading the privacy policy of any app before connecting it to financial accounts is not optional. It is a basic consumer protection step that most users skip.

The CFPB’s consumer financial data rights guidance at consumerfinance.gov explains your rights regarding how financial companies can use your data under current US regulations. These regulations are evolving as the Consumer Data Protection Act debate continues in Congress as of 2026.

Where This Is Heading: The Next Three Years

Several developments that are currently emerging in AI and personal finance are likely to become mainstream by 2028. Understanding them now gives consumers time to make informed decisions rather than reactive ones.

Hyper-personalized financial products

The direction of AI in lending, insurance, and investment management is toward products customized at the individual level rather than the tier level. A health insurance premium that updates monthly based on wearable device data. A car insurance rate that adjusts daily based on driving behavior. A mortgage rate that reflects the specific risk profile of the borrower rather than a band. The consumer benefit is that more accurately priced products. The consumer risk is increased surveillance of behavior and the potential for pricing discrimination that is difficult to detect or challenge.

Embedded AI financial advice in everyday apps

The clearest near-term trend is AI financial guidance moving into the apps and platforms where Americans already spend time, not requiring a separate financial app to be opened. Apple’s financial features, Google’s financial integrations and the AI layers being built into major banks’ mobile apps all point toward a world where financial guidance is contextual and ambient rather than requiring deliberate navigation to a financial planning tool.

Regulatory development: still catching up

The regulatory framework governing AI in US financial services is materially behind the technology. The CFPB has issued guidance on AI credit decisions and data rights. The SEC has begun examining AI use in investment advice. But comprehensive federal regulation of AI in consumer financial services does not yet exist as of 2026. The patchwork of existing regulations, including ECOA, FCRA and the Investment Advisers Act, was not designed for AI systems and leaves significant gaps in consumer protection.

Americans who understand these gaps are better positioned to advocate for their interests in credit decisions, to question AI-generated financial recommendations and to make informed choices about which apps receive access to their financial data.

What Americans Should Do Right Now

The AI shift in personal finance is already underway. The question is not whether to engage with it but how to do so in a way that captures the benefits while managing the risks.

Five practical actions to take in 2026

- Understand what AI tools you are already using. Log into your bank app, your credit card account and any financial app on your phone. Identify whether AI is being used for fraud detection, spending analysis or credit decisioning. Most apps disclose this in their terms, though it requires reading them.

- Take advantage of AI fraud protection actively. Ensure all contact information is current with every financial institution. Enable push notification alerts for all transactions above $1. The AI catches the fraud, but you need to be reachable to confirm or deny it quickly.

- Use robo-advisors to start investing if you have not already. The access barrier to professionally managed investment portfolios is lower than it has ever been. For Americans not currently invested, the cost of inaction compounds over time. Fidelity Go and SoFi Automated Investing are free starting points with no minimum balance.

- Read privacy policies before connecting apps to financial accounts. This takes 10 minutes and gives you specific knowledge about how your transaction data can be used. If a privacy policy permits sharing data with third-party marketers, consider whether the app’s value justifies that access.

- Know when AI is not enough and seek human guidance. Use AI tools for financial education, budgeting, and routine investment management. Consult a licensed professional for tax planning, retirement income sequencing, major financial decisions, and any situation where the financial stakes and complexity exceed what a general AI tool can reliably handle. Free certified financial counseling is available through the NFCC at no cost.

Frequently Asked Questions

Is AI making financial advisors obsolete?

Not entirely, but AI is changing what human advisors need to do to justify their cost. Routine portfolio management, basic budgeting guidance, and standard retirement savings advice are all being handled more efficiently and cheaply by AI tools. Where human advisors retain clear value is in complex situations, in behavioral coaching during market volatility, and in the integrated planning that spans tax, investment, insurance, and estate decisions simultaneously. The advisors who are most at risk are those whose practices rely primarily on standard products rather than genuinely personalized, complex advice.

Can AI give better financial advice than a human?

In narrow, well-defined domains such as portfolio rebalancing, tax-loss harvesting, and fraud detection. AI outperforms human manual processes on speed, consistency, and cost. In complex, holistic personal financial planning, particularly decisions involving life events, competing priorities, and emotional dimensions. Human advisors who know their clients well continue to provide value that AI cannot replicate. The honest answer is that it depends entirely on what ‘better financial advice’ means in a given situation.

Is my financial data safe with AI-powered apps?

It depends on the app and how you define safe. Major platforms including Betterment, Wealthfront, Credit Karma and Copilot use bank-level encryption for data transmission and are regulated by the SEC, FINRA or both. The practical security risk is low. The data privacy risk, which is how the company uses your financial transaction data commercially, which is a separate question that requires reading the privacy policy of each app individually. These are two different concerns that are often conflated.

Does AI in lending make it easier or harder to get a loan?

Both, depending on the borrower profile. Americans with strong repayment behavior but thin credit files, such as recent graduates, new immigrants and self-employed individuals, may find it easier to qualify for credit through AI lenders that assess actual financial behavior rather than just bureau scores. Americans who have had financial difficulties in the past may find that AI models surface those difficulties more precisely than a human underwriter applying manual judgement. The net effect on access depends heavily on the individual’s specific financial history.

What regulations protect Americans from unfair AI financial decisions?

The Equal Credit Opportunity Act requires that AI credit decisions be explainable and non-discriminatory. The Fair Credit Reporting Act governs how AI uses consumer credit data. The CFPB has issued guidance on AI credit decisioning and consumer rights. However, comprehensive federal AI-specific financial regulation does not yet exist as of 2026. Consumers who believe an AI credit decision was unfair can file a complaint with the CFPB at consumerfinance.gov/complaint.

| AI in personal finance is not a story about technology replacing people. It is a story about access. The financial tools, portfolio management and real-time fraud protection that were once available only to wealthy Americans with expensive advisors are now embedded in free apps available to anyone with a smartphone. What you do with that access, and how carefully you manage the data and decisions that come with it, is the more important question. |

Conclusion

AI has already changed personal finance for everyday Americans in six concrete ways: faster and broader credit decisions, dramatically more effective fraud detection, democratized investment management, predictive spending analysis, personalized lending and accessible financial guidance through conversational AI.

Each of these changes carries both benefits and risks that exist simultaneously. AI credit decisions expand access for some borrowers and introduce bias risks for others. AI fraud detection is the most unambiguously beneficial change for consumers. Robo-advisors have lowered the barrier to investing to its lowest point in American financial history. Predictive budgeting is more useful than reporting, but only for households whose spending is primarily card-based. AI lending accelerates access at the cost of reducing the natural friction that protects impulsive borrowers. Conversational AI provides unprecedented financial education access with real risks from confident-sounding incorrect answers.

The Americans who benefit most from the AI shift in personal finance are those who understand what each tool does, what it does not do and where to turn when a situation exceeds what any AI can handle. For ongoing practical guidance on specific AI tools, our review of the best AI money-saving tools in 2026 and our guide to AI investing apps for beginners cover the specific platforms in detail.

| 📥 Free Download: AI Personal Finance Readiness Checklist A practical worksheet to assess which AI financial tools are relevant to your current situation and which to prioritize first. Includes: ✔ AI tool readiness assessment: match tools to your financial stage ✔ Data privacy checklist: what to check before connecting any app ✔ AI vs human advisor decision guide: when to use which Free. Email required. Educational reference tool only. |

| 📲 Share This Article If this analysis helped you understand the AI shift in personal finance, share it with someone who should know. Share on WhatsApp, Facebook or by text message. Thank you for reading TechAIFinance.com. |

Read Next

Continue exploring AI and personal finance on TechAIFinance.com:

- Best AI Tools to Help You Save Money in 2026

- Best AI Investing Apps for Beginners in the US 2026

- How to Use ChatGPT to Create a Personal Budget

- How to Use AI to Get Out of Debt Faster

- What Kills Your FICO Credit Score Without You Knowing

| ✍ About the Author Written by: TechAIFinance Editorial Team Edited and Fact-Checked by: Olayinka Adejugbe Olayinka Adejugbe is not a licensed financial advisor. The content on TechAIFinance.com is produced for educational purposes only and should not be treated as personalized financial advice. Olayinka is the founder and lead editor of TechAIFinance.com. He holds a Global Certification in Artificial Intelligence and Applied Innovation and an Award of Completion in Behavioral Counseling from the World Health Organization. With a strong working knowledge of personal finance and accounting principles, Olayinka oversees the editorial review of every article on this site to ensure accuracy, currency and practical usefulness. Every article on TechAIFinance.com is produced by our research team and reviewed by Olayinka before publication. We verify statistics against named authoritative sources and update content when circumstances change. Visit our About page to learn more about our editorial process. Use our Contact page to get in touch. |

Important Disclaimer

The content published on TechAIFinance.com is for educational and informational purposes only. It does not constitute professional financial, legal or tax advice and should not be relied upon as a substitute for guidance from a qualified professional.

Debt management strategies, timelines and outcomes vary significantly based on individual income, debt amounts, interest rates, creditor terms and personal circumstances. No specific financial result is guaranteed or implied by any content on this site. Always consult a qualified financial advisor, credit counselor or attorney before making significant financial decisions. Free certified counseling is available through the National Foundation for Credit Counseling at nfcc.org.