| Disclaimer: Life insurance is a regulated financial product. This article is for educational purposes only and does not constitute insurance, financial or legal advice. Coverage needs, policy suitability and premium costs vary significantly by individual health, age, income, family situation and state of residence. Always consult a licensed insurance professional or independent broker before purchasing any life insurance policy. The information in this guide is intended to help you understand the landscape before that conversation, not to replace it. |

| ℹ Quick Summary According to a 2023 LIMRA and Life Happens study, approximately 52 percent of Americans reported having life insurance coverage, leaving nearly half of the adult population without any protection for their dependents. Among those without coverage, the most commonly cited reasons were uncertainty about how much coverage is needed, confusion about which type to buy and concern about cost. This guide addresses all three. It explains how the main policy types work, how to estimate a coverage figure that reflects your household’s actual obligations and what questions to ask before making a decision. |

| 📘 What You’ll Learn In this educational guide you will find: A clear explanation of the three main life insurance types available in the US How to estimate how much coverage your household may need A comparison of term, whole and universal life across cost, flexibility and use case The factors that affect premiums and what underwriting involves Questions to ask an insurance agent or independent broker Free resources for comparing quotes and understanding policy terms |

Table of Contents

- What Life Insurance Is and Who Needs It

- The Three Main Types of Life Insurance in the US

- Term Life Insurance: How It Works

- Whole Life Insurance: How It Works

- Universal Life Insurance: How It Works

- Side-by-Side Comparison of All Three Types

- How to Estimate How Much Coverage You May Need

- Factors That Affect Your Premium

- How the Underwriting Process Works

- Questions to Ask Before Buying

- Where to Compare Life Insurance Quotes in the US

- Frequently Asked Questions

What Life Insurance Is and Who Needs It

Life insurance is a contract between a policyholder and an insurance company. The policyholder pays a regular premium. In exchange, the insurer agrees to pay a defined sum, being the death benefit, paid to named beneficiaries upon the policyholder’s death.

The fundamental purpose is income replacement and financial protection for people who depend on the policyholder financially. When a primary earner dies, the household loses income that may have been covering mortgage payments, childcare, education costs, daily living expenses and outstanding debt. Life insurance is designed to bridge that gap for a defined period or permanently, depending on the policy type chosen.

Who generally benefits from life insurance: people with financial dependents, such as a spouse, children or other family members who rely on their income, and people with shared financial obligations such as a joint mortgage or co-signed debt. Single individuals with no dependents and no shared debts have less immediate need for life insurance, though some purchase it for estate planning purposes or to lock in premiums at a younger age.

According to the 2023 LIMRA Insurance Barometer Study, the median life insurance ownership gap, which is the difference between what Americans have and what they say they need, has been widening for over a decade. Cost and complexity are the primary barriers, both of which this guide addresses.

The Three Main Types of Life Insurance in the US

Most Americans choosing life insurance are selecting from three policy structures. Each works differently, costs differently and suits different financial situations.

Understanding the core difference between them before speaking with an agent prevents the most common mistake in life insurance purchasing, which is choosing the wrong type for your actual needs because the sales presentation emphasized one product over others.

Term Life Insurance: How It Works

Term life insurance provides coverage for a defined period, typically 10, 15, 20 or 30 years. If the insured person dies during the term, the death benefit is paid to beneficiaries. If the term expires and the insured is still living, the policy ends with no payout and no cash value returned.

Term is the simplest and least expensive form of life insurance. For a healthy non-smoking 35-year-old, a 20-year term policy with a $500,000 death benefit typically costs between $25 and $40 per month, according to 2024 rate data from Policy genius.

When Term Life Is Often Appropriate

- Households with young children who need income protection through the child-rearing years

- Homeowners with a mortgage, where the term can be matched to the mortgage duration

- Borrowers with significant debt that a surviving spouse or co-signer would be responsible for

- Income earners who want maximum coverage at minimum cost during peak earning and responsibility years

- People who plan to self-insure through investment and asset accumulation by the time the term expires

What Term Life Does Not Provide

- No cash value builds within the policy. Premiums do not accumulate a savings component

- Coverage ends when the term expires. Renewing at an older age typically means significantly higher premiums

- No permanent death benefit. If the insured outlives the term, beneficiaries receive nothing

| 💡 Pro Tip Level term policies, where the premium stays the same for the entire term, are the most straightforward and most commonly purchased form. Avoid annually renewable term policies for long-term coverage needs. Premiums increase each year as age increases, making them expensive over a 20-year horizon compared to a fixed-premium level term policy. |

Whole Life Insurance: How It Works

Whole life insurance provides coverage for the insured’s entire lifetime rather than a fixed term, as long as premiums continue to be paid. It also includes a cash value component that accumulates over time at a guaranteed minimum rate and can be borrowed against or surrendered.

The premium for whole life is significantly higher than term for the same death benefit. For the same healthy 35-year-old, a $500,000 whole life policy might carry a premium of $400 to $600 per month, roughly 10 to 20 times the cost of an equivalent term policy, according to industry rate data from the American Council of Life Insurers 2023 report.

When Whole Life May Be Worth Considering

- Estate planning situations where leaving a guaranteed death benefit regardless of lifespan is the primary objective

- Households where the insured has a lifelong financial dependent, such as a child with a disability, who will always require financial support

- Business continuity planning where a death benefit needs to be permanently guaranteed

- High-net-worth individuals using whole life as part of a broader tax and estate planning strategy under guidance from a financial advisor

What Whole Life Does Not Provide for Most Households

- The cash value growth rate in whole life policies is typically modest, often 1 to 2 percent in guaranteed crediting, according to the National Association of Insurance Commissioners 2023 data, and does not match the long-term returns available through index funds or other investment vehicles

- The high premium cost means many households are either underinsured for their actual coverage needs or overcommitted relative to their budget

- Surrendering the policy early typically results in surrender charges that reduce or eliminate the cash value

| ⚠ Watch Out Whole life insurance is frequently sold in contexts where term life would serve the coverage need more efficiently and at significantly lower cost. The cash value component is often presented as an investment benefit. For most households, the combination of a term policy for coverage needs plus a separate retirement account for investment purposes produces better financial outcomes than whole life at a lower total cost. This is a general observation, not a universal rule. Some situations genuinely warrant whole life. An independent fee-only financial advisor can help assess whether your situation is one of them. |

Universal Life Insurance: How It Works

Universal life insurance sits between term and whole life in both structure and cost. Like whole life, it is a permanent policy that builds cash value. Unlike whole life, it offers flexibility. The policyholder can adjust premium payments and death benefit amounts within defined limits as financial circumstances change.

The cash value in a universal life policy earns interest based on a rate tied to a market index or set by the insurer, rather than a fixed guaranteed rate. This creates more growth potential than whole life but also more variability.

Variations Within Universal Life

- Guaranteed Universal Life (GUL): focuses on a permanent death benefit with minimal cash value. Premiums are lower than whole life. Suitable for those who want lifelong coverage without the investment component.

- Indexed Universal Life (IUL): cash value growth is tied to a market index such as the S&P 500, with a floor that limits losses. More growth potential than whole life, but policy structure can be complex and costs vary significantly between insurers.

- Variable Universal Life (VUL): cash value is invested directly in market subaccounts. Highest growth potential but also the most risk. Cash value can decrease in a market downturn, which can affect the policy’s sustainability.

Universal life policies, particularly IUL and VUL products, carry complexity that warrants careful review of policy illustrations and independent professional advice before purchase.

Side-by-Side Comparison of All Three Types

| Feature | Term Life | Whole Life | Universal Life |

| Coverage period | Fixed term: 10 to 30 years | Lifetime (if premiums paid) | Lifetime (if funded correctly) |

| Monthly cost (example) | $25 to $40 for $500K | $400 to $600 for $500K | $100 to $300+ for $500K |

| Cash value | None | Yes: guaranteed rate | Yes: variable or indexed |

| Premium flexibility | Fixed | Fixed | Adjustable within limits |

| Death benefit flexibility | Fixed | Fixed | Adjustable within limits |

| Best suited to | Income replacement, mortgage, family protection | Estate planning, permanent dependents | Flexible permanent coverage needs |

| Complexity | Low | Moderate | High |

Premium figures in this table are illustrative estimates for a healthy non-smoking 35-year-old American based on publicly available industry rate data as of early 2026. Actual premiums depend on age, health, gender, state of residence, insurer, and specific policy terms.

How to Estimate How Much Coverage You May Need

Determining an appropriate coverage amount requires understanding what the death benefit is intended to replace or cover. There is no single formula that applies to every household, but several widely used estimation frameworks provide a useful starting point.

The DIME Method

The DIME framework is one of the more comprehensive estimation approaches used by financial educators and insurance professionals. It stands for Debt, Income, Mortgage, and Education.

- D: Debt: the total of all outstanding debts excluding the mortgage, including credit cards, personal loans, student loans, and car loans, that dependents would be responsible for

- I: Income: your annual income multiplied by the number of years your dependents would need financial support. For a household with young children, this is often 10 to 20 years

- M: Mortgage: the outstanding balance on your home loan, so dependents are not at risk of losing the home

- E: Education: an estimate of future education costs for children, if applicable

Adding these four figures gives a total coverage estimate. It is not a precise calculation, as income replacement years involve assumptions and education costs are uncertain, but it provides a more grounded starting point than rules of thumb like ‘ten times your salary.’

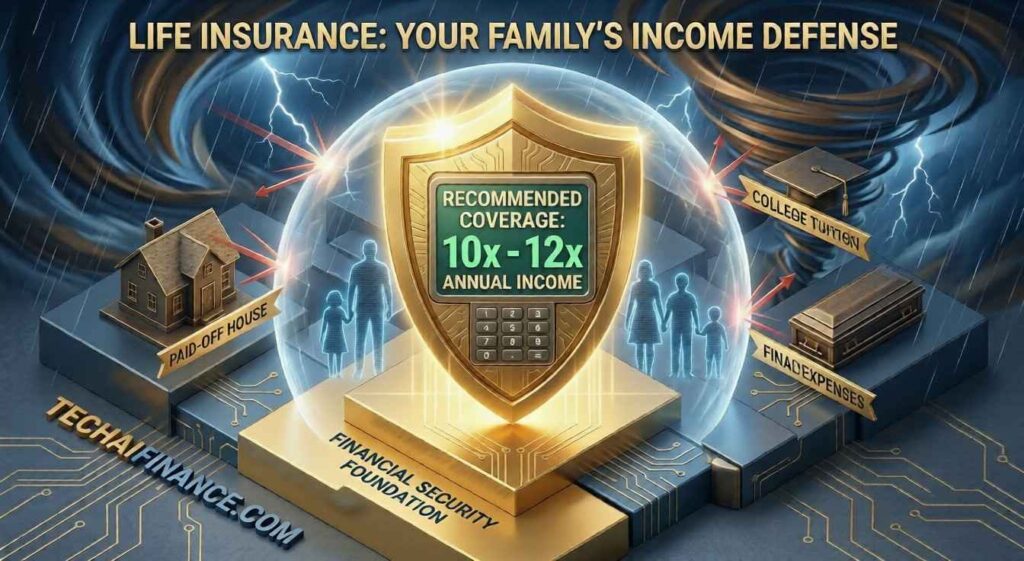

A Simplified Rule of Thumb

For households that want a quicker estimate, multiplying gross annual income by 10 to 12 is the most commonly cited rule of thumb in US financial education materials. The Insurance Information Institute uses this range as a general reference. It is less precise than DIME but gives a working figure to take into an insurance conversation.

| Illustrative Example: A 38-year-old married parent of two in Minnesota earns $68,000 per year. Using the DIME method: $22,000 in non-mortgage debt, 15 years of income replacement at $68,000 = $1,020,000, $187,000 remaining mortgage balance, $60,000 estimated education costs for two children. Total estimate: approximately $1,289,000. Using the 10x rule: $68,000 x 10 = $680,000. The DIME method produces a meaningfully higher figure in this scenario because it accounts for specific obligations rather than a flat income multiple. Individual results will vary based on actual debt levels, income and family circumstances. |

Factors That Affect Your Premium

Life insurance premiums are calculated through a process called underwriting, where the insurer assesses the risk of insuring a specific individual. Understanding the factors involved helps you anticipate where your premium is likely to land and what steps, if any, might improve your rate.

Primary Underwriting Factors

- Age: the most significant single factor. Premiums increase with age because mortality risk increases. Purchasing at a younger age locks in a lower rate for the full policy term.

- Health status: current health conditions, medical history, height and weight relative to actuarial tables, blood pressure, and cholesterol levels all affect the rate classification assigned

- Tobacco use: smokers typically pay two to three times the premium of non-smokers for equivalent coverage. Most insurers define tobacco use broadly to include cigarettes, cigars, chewing tobacco, and some vaping products

- Family medical history: a family history of certain conditions, such as heart disease, cancer, or diabetes, before age 65, may affect rate classification even if the applicant is currently healthy

- Occupation and hobbies: high-risk occupations such as commercial fishing, logging, and roofing, and high-risk hobbies such as private aviation or extreme sports, can increase premiums or result in policy exclusions

- Gender: Actuarial data show women have longer average lifespans than men in the US. In most states, this results in lower premiums for women for the same coverage amount

Rate Classifications

Insurers assign applicants to rate classifications that determine the premium. The classifications vary by insurer but typically follow a structure similar to: Preferred Plus or Super Preferred (best rates, excellent health), Preferred, Standard Plus, Standard, and Substandard or Rated (higher premiums for elevated risk factors).

Receiving a Preferred Plus classification rather than a Standard classification can reduce the premium by 40 to 60 percent for the same coverage amount, according to pricing data from the American Council of Life Insurers. If you are in good health, it is worth understanding what each insurer’s criteria are for their best classification before applying.

How the Underwriting Process Works

After submitting a life insurance application, the underwriting process begins. The length and intensity of underwriting depend on the coverage amount and the insurer’s requirements.

Traditional Full Underwriting

For larger coverage amounts, typically above $500,000, full underwriting is common. This typically involves a paramedical exam conducted at your home or a testing center, including blood draw, urine sample, blood pressure, and height and weight measurement. Medical records may be requested from your physician. The process typically takes 4 to 8 weeks.

Accelerated or Simplified Underwriting

Many insurers now offer accelerated underwriting for coverage amounts below $1 million to $3 million (thresholds vary by insurer). Instead of a medical exam, the insurer reviews existing data sources, including MIB (Medical Information Bureau) records, prescription drug databases, motor vehicle records and credit information, to make an underwriting decision. This can reduce the approval timeline to days or hours.

No-Exam or Simplified Issue Policies

Some insurers offer policies that require no medical exam and only a brief health questionnaire. These are typically available for smaller coverage amounts and carry higher premiums than fully underwritten policies because the insurer is accepting more risk without detailed health data. They may be appropriate for individuals who cannot qualify for standard underwriting due to health conditions.

Questions to Ask Before Buying

Whether you are working with a captive agent representing one insurer or an independent broker with access to multiple carriers, these questions help ensure you understand what you are purchasing.

- What type of policy is this, and why is it recommended for my situation? Ask the agent to explain specifically why this product suits your coverage needs better than alternatives.

- What is the total cost over the full policy term? For term policies, this is the premium multiplied by months. For permanent policies, request a full illustration of projected costs and values over 20 and 30 years.

- What is the insurer’s financial strength rating? Look for ratings from AM Best, Moody’s, or Standard and Poor’s. A rating of A or above from AM Best is generally considered solid. This matters because you are entering a contract that may run for decades.

- What happens if I miss a premium payment? Understand the grace period and what triggers policy lapse.

- Are there any exclusions I should know about? Common exclusions include suicide within the first two years of the policy and death resulting from activities disclosed as high-risk during underwriting.

- For permanent policies: what are the guaranteed values versus illustrated values? Illustrations often show projected values based on assumed interest rates that are not guaranteed. Ask specifically for the guaranteed minimum values.

- Is this agent independent or captive? A captive agent represents one insurer and can only offer that insurer’s products. An independent broker can compare multiple insurers and is often better positioned to find the most competitive rate for your health profile.

Where to Compare Life Insurance Quotes in the US

Several legitimate platforms allow US consumers to compare term life insurance quotes from multiple insurers without purchasing immediately.

- Policygenius: policygenius.com: independent broker platform comparing quotes from over 30 US insurers. No purchase required to view quotes. Licensed agents available for guidance.

- Ladder: ladderlife.com: online term life platform with instant coverage decisions for eligible applicants. No medical exam for qualifying amounts. tab.

- Bestow: bestow.com: tech-based term life insurer offering accelerated underwriting with no medical exam requirement.

- Haven Life: havenlife.com: term life platform backed by MassMutual. Offers instant decisions for eligible applicants.

- NAIC Consumer Information: content.naic.org/sites/default/files/publication-lha-pb-life-insurance-basics.pdf: The National Association of Insurance Commissioners provides free consumer guides to understanding life insurance in the US.

Comparison platforms show indicative quotes based on basic information. Final premiums are determined after underwriting. Use multiple platforms to see a range before committing to a specific insurer.

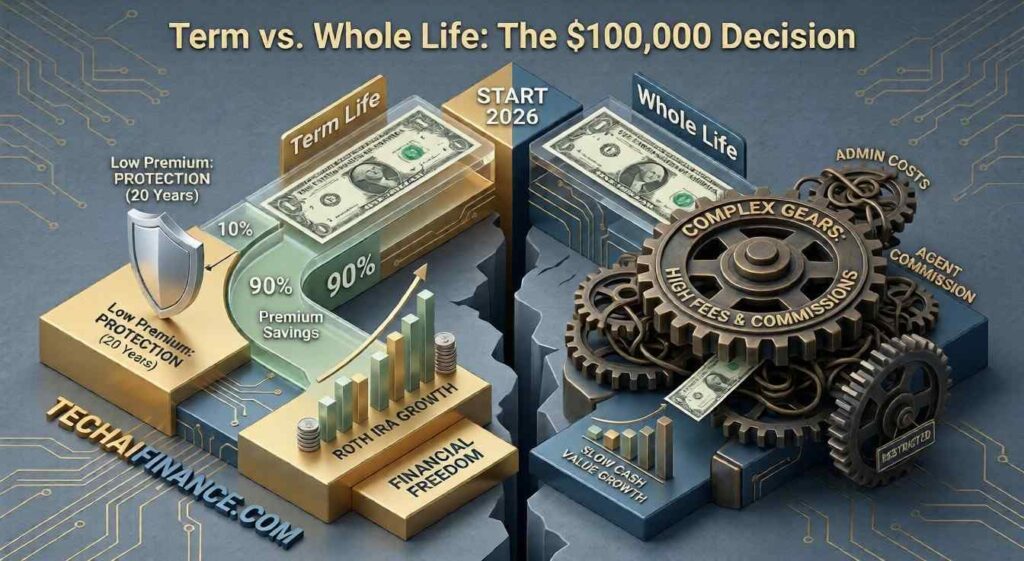

An Illustrative Decision Example: Term vs Whole Life

| Illustrative Example: Not a Guarantee or Recommendation Consider a hypothetical 32-year-old non-smoking married parent in Ohio with two young children, a $230,000 mortgage, and an annual income of $72,000. Their primary goal is to ensure their family can maintain their home and lifestyle for 20 years if they were to die unexpectedly. Option A: A 20-year term policy with an $800,000 death benefit at a quoted premium of $38 per month. This covers the mortgage balance, provides income replacement for the term, and covers an estimated portion of future education costs. The policy ends at age 52. Option B: A whole life policy with an $800,000 death benefit at $520 per month. This provides permanent coverage and a cash value component growing at approximately 1.5 percent per year. The annual premium difference is $5,784. If that difference were invested at a 7 percent average annual return over 20 years in a tax-advantaged retirement account, the projected accumulated value would exceed $250,000, significantly more than the projected cash value of the whole life policy over the same period. This example is illustrative only. It does not account for individual tax situations, health classifications, state-specific premiums or investment returns that may differ from the assumed rate. Consult a licensed insurance professional and an independent financial advisor before making any policy decision. |

Frequently Asked Questions

How much life insurance do most Americans actually need?

Coverage needs vary significantly by household situation. The LIMRA Insurance Barometer Study consistently finds that Americans with coverage often have less than they estimate they need. Using the DIME method or a 10 to 12 times income estimate provides a starting point, but the most accurate figure comes from a detailed needs analysis conducted with a licensed insurance professional who understands your specific obligations, income and family situation.

Is term life insurance always the better choice?

For the majority of Americans whose primary need is income replacement and debt protection during peak family responsibility years, term life tends to offer the most coverage at the lowest cost. However, it is not universally superior. Certain estate planning situations, business continuity needs and lifelong dependent circumstances may genuinely warrant permanent coverage. The right answer depends on individual circumstances.

At what age should I buy life insurance?

Premiums increase with age because mortality risk increases actuarially. Purchasing at a younger age and in good health locks in a lower rate for the policy duration. For families with young children and a mortgage, the most common recommendation from financial educators is to secure coverage in the 25 to 40 age range while premiums are at their most accessible levels.

What is the free look period?

Federal regulations and most state insurance laws require insurers to provide a free look period, typically 10 to 30 days, after a policy is delivered during which the policyholder can review the terms and cancel for a full premium refund if they are not satisfied. Always review the policy document carefully during this period before considering it final.

Can I have more than one life insurance policy?

Yes. Many Americans hold multiple policies, for example, a term policy for mortgage and income replacement combined with a smaller whole life policy for final expenses. Insurers may ask about existing coverage during underwriting. Total coverage across all policies should reflect genuine financial need rather than exceed it significantly, as insurers may decline coverage they consider excessive relative to financial justification.

Where can I get free help understanding life insurance in the US?

- National Association of Insurance Commissioners (NAIC): free consumer guides and a tool for finding your state’s insurance department. Opens in new tab.

- NAIC Shopper’s Guide to Life Insurance: the official government consumer guide to understanding life insurance products. Opens in new tab.

- Insurance Information Institute: free educational resources on all types of personal insurance in the US. Opens in new tab.

| The most expensive life insurance decision most Americans make is not choosing the wrong policy type. It is delaying the decision entirely. Premiums are lowest when coverage is purchased young and in good health. The cost of waiting is real and measurable. |

Conclusion

Choosing the right life insurance plan starts with understanding what the policy is for, whether income replacement, debt coverage, mortgage protection or permanent estate planning, and matching the policy structure to that specific purpose.

For most American households with dependents and a mortgage, term life insurance delivers the most coverage at the most accessible cost. Whole and universal life serve genuine purposes in specific situations but carry complexity and cost that warrant careful independent evaluation.

Estimating coverage needs through the DIME method, comparing quotes through independent platforms, and working with a licensed professional who can explain the underwriting classification you receive are the three most practical steps toward making a well-informed decision.

The National Association of Insurance Commissioners at naic.org provides free consumer guidance and a tool for verifying that any agent or broker you work with is licensed in your state. This verification step is worth taking before committing to any policy.

| 📥 Free Download: Life Insurance Needs Assessment Worksheet A practical educational tool to help you estimate your coverage needs before speaking with an insurance professional. Includes: ✔ Income replacement calculator: estimate how much coverage your dependents may need ✔ Debt and obligation summary: mortgage, loans and final expenses ✔ Policy comparison grid: term vs whole vs universal side by side Free. Email required. Educational purposes only. Always consult a licensed insurance professional for personalized recommendations. |

| 📲 Share This Article If this guide has been useful, consider sharing it with a family member or colleague who is thinking about life insurance. Share on WhatsApp, Facebook or by text message. Thank you for reading TechAIFinance.com. |

Read Next

Continue building your financial knowledge on TechAIFinance.com:

- How to Build an Emergency Fund From Zero

- How to Create a Budget When Living Paycheck to Paycheck

- How to Get Out of Debt on a Low Income in the US

- Best AI Tools to Help You Save Money in 2026

- How to Save Money on a Tight Budget: 20 Practical Tips

| ✍ About the Author Written by: TechAIFinance Editorial Team Edited and Fact-Checked by: Olayinka Adejugbe Olayinka Adejugbe is not a licensed financial advisor. The content on TechAIFinance.com is produced for educational purposes only and should not be treated as personalized financial advice. Olayinka is the founder and lead editor of TechAIFinance.com. He holds a Global Certification in Artificial Intelligence and Applied Innovation and an Award of Completion in Behavioral Counseling from the World Health Organization. With a strong working knowledge of personal finance and accounting principles, Olayinka oversees the editorial review of every article on this site to ensure accuracy, currency and practical usefulness. Every article on TechAIFinance.com is produced by our research team and reviewed by Olayinka before publication. We verify statistics against named authoritative sources and update content when circumstances change. Visit our About page to learn more about our editorial process. Use our Contact page to get in touch. |

Important Disclaimer

The content published on TechAIFinance.com is for educational and informational purposes only. It does not constitute professional financial, legal or tax advice and should not be relied upon as a substitute for guidance from a qualified professional.

Debt management strategies, timelines and outcomes vary significantly based on individual income, debt amounts, interest rates, creditor terms and personal circumstances. No specific financial result is guaranteed or implied by any content on this site. Always consult a qualified financial advisor, credit counselor or attorney before making significant financial decisions. Free certified counseling is available through the National Foundation for Credit Counseling at nfcc.org.