| Disclosure and Content Note This guide provides information about income strategies for Americans during economic downturns. It is not financial, investment or employment advice. Income results vary based on individual skills, location, market conditions and effort. Some links may be affiliate links. All platform details and earning figures were verified in April 2026. |

A recession does not feel the same for every American. For some it means a pay cut or reduced hours. For others it means a layoff with no warning. For those still employed it means watching friends struggle while their own anxiety quietly grows. Regardless of where you sit, a recession forces the same question: how do I protect my income and financial stability when the economy is working against me?

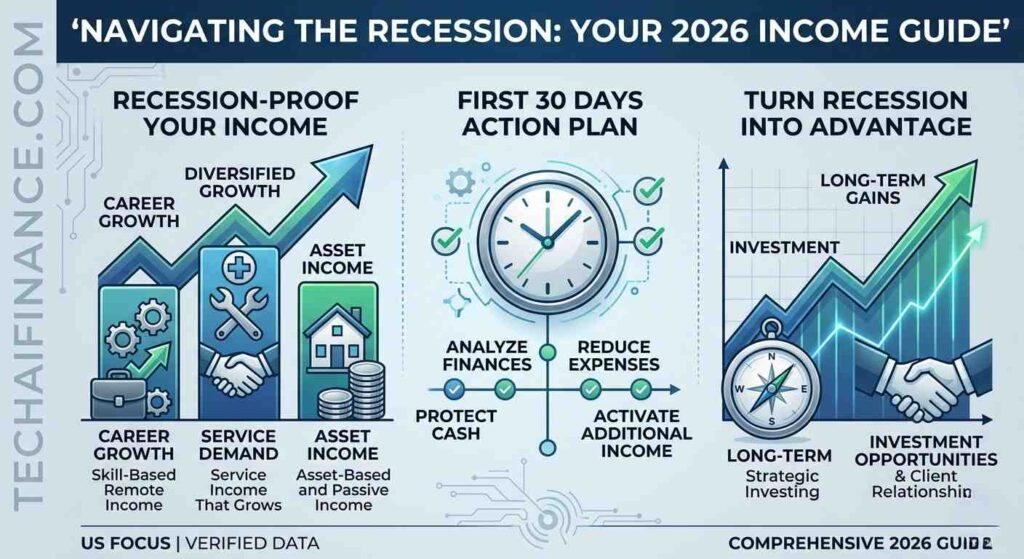

The answer is not to panic and not to wait passively. The Americans who navigate recessions most successfully are the ones who act quickly to diversify their income before a single source disappears, cut spending to what genuinely matters and position themselves to take advantage of the opportunities that every recession creates alongside its hardships.

Recessions do create opportunities. Demand for specific services rises dramatically as people and businesses try to reduce costs. Skilled workers who make themselves available during downturns often build client relationships that sustain their income long after conditions improve. The recession strategy that works is about building an income structure more resilient than the one you had before.

This guide covers 12 specific income strategies for Americans during a recession, each selected because it either remains stable or grows in demand during economic downturns and can be started without significant upfront capital.

| ℹ Quick Summary Recessions and US income: what the data shows Average US recession since World War II: approximately 10 months, per National Bureau of Economic Research. Americans with multiple income sources experienced 47 percent lower financial hardship during the 2020 recession than those with a single income source, per Federal Reserve SHED Report 2020. Sectors that grew or stayed stable during the 2008 and 2020 recessions: healthcare, essential retail, debt counseling, home repair, online education and government services. Americans who invested during the March 2020 market low and held through December 2021 saw average portfolio gains exceeding 100 percent on those purchases. Sources: National Bureau of Economic Research at nber.org. Federal Reserve SHED Report 2020 at federalreserve.gov. |

| 📘 What This Guide Covers In this guide you will find: 12 recession-proof income strategies fully explained for Americans in 2026 Why each strategy holds up or grows during economic downturns Realistic earning ranges based on verified data not marketing claims How AI tools make each strategy faster to execute The specific financial actions to take in the first 30 days of a recession How to cut expenses without destroying your quality of life How to turn a recession into a long-term financial advantage |

Table of Contents

- How to Think About Income During a Recession

- The First 30 Days: Immediate Financial Actions

- Category 1: Service Income That Grows in Recessions

- Category 2: Skill-Based Remote Income

- Category 3: Asset-Based and Passive Income

- Category 4: Recession Investment Opportunities

- How to Cut Expenses Without Cutting Your Life

- Recession-Proofing Your Income for the Long Term

- Full Strategy Comparison Table

- Frequently Asked Questions

How to Think About Income During a Recession

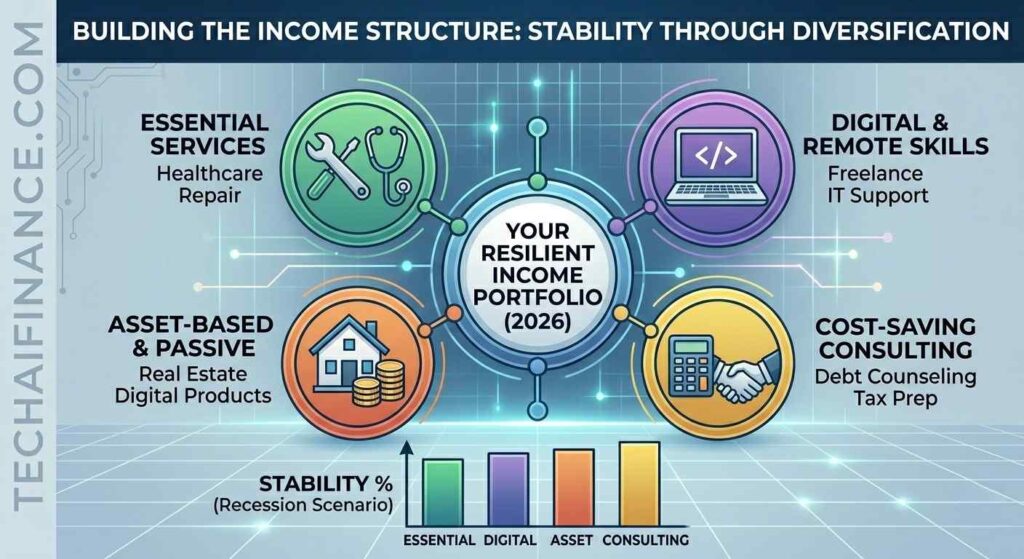

The first mental shift during a recession is moving from thinking about income as a single stream to thinking about it as a portfolio. A single income source creates a binary outcome: it either continues or stops. A portfolio of income sources creates a graduated outcome where some streams may be reduced while others remain stable or grow. This diversification principle is the same logic that drives investment portfolio diversification. Applied to income, it means the loss of one source does not produce financial collapse when other sources continue.

Three types of recession-resilient income

Essential service income

Income from services people need regardless of economic conditions: healthcare, childcare, food, utilities, basic home repair and financial counseling all maintain or increase demand during recessions because these are needs rather than wants.

Cost-saving service income

Income from helping people and businesses spend less money. Financial coaching, tax preparation, debt counseling and IT support see demand rise during recessions because people who previously ignored inefficiencies now need to find savings urgently.

Digital and remote income

Income from digital skills that do not depend on local economic conditions. Freelance work, online tutoring and digital product sales are sourced globally. An American freelancer whose city is suffering can still find clients in cities where conditions are better.

| ⭐ Key Takeaway The most important financial action before a recession is diversifying your income before you need to. Every American who has been laid off has thought the same thing afterward: I wish I had started building that second income stream six months ago. The best time to build recession-proof income is when your primary income is stable. The second best time is right now. Source: Federal Reserve SHED Report 2020, which found income diversity was the strongest predictor of financial resilience during the COVID recession. |

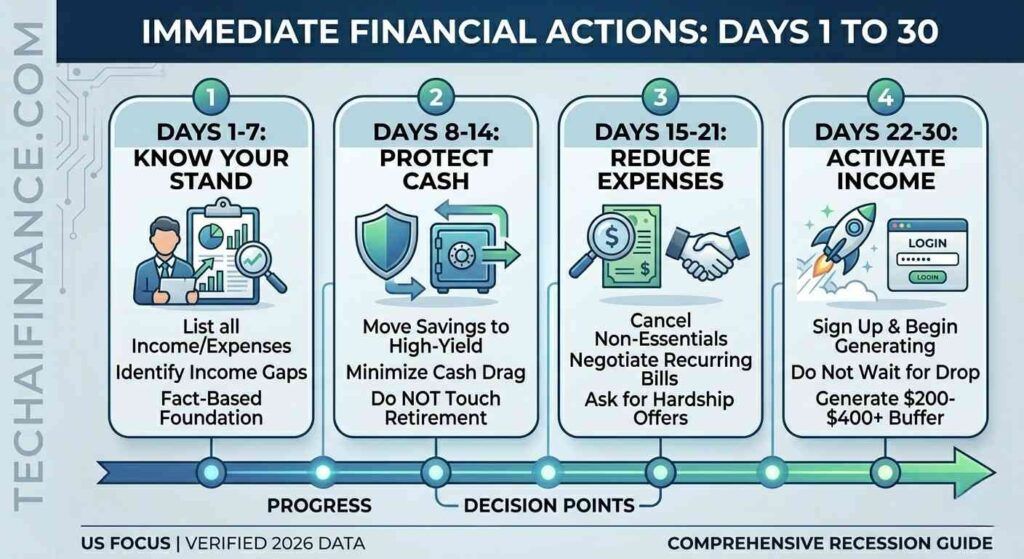

The First 30 Days: Immediate Financial Actions

When a recession begins or when your personal situation deteriorates, the first 30 days of response matter more than anything else.

Days 1 to 7: Know exactly where you stand

Calculate your exact financial position before making any changes. List every income source and its monthly amount. List every fixed expense. Identify the gap between the two under current conditions and under a scenario where your primary income is reduced by 25 or 50 percent or eliminated. This exercise takes two to three hours and produces the factual foundation every subsequent decision needs.

Days 8 to 14: Protect your cash position

Move all savings above your operating minimum to the highest-yield savings account available. Do not touch retirement accounts unless absolutely necessary because early withdrawal penalties and taxes reduce the accessible value by 30 to 40 percent and permanently remove money from long-term wealth building.

Days 15 to 21: Reduce recurring expenses immediately

Cancel or negotiate every monthly charge that is not essential to your income or basic living requirements. Call your internet provider, insurance company and phone carrier and ask directly for a better rate or temporary hardship accommodation. Many providers have undisclosed retention offers for customers who ask. The average American household has $200 to $400 per month in cancellable or negotiable recurring charges.

Days 22 to 30: Activate additional income immediately

Do not wait for your primary income to drop before activating additional streams. Sign up for one platform from this guide that matches your current skills and begin generating income this month. Even $200 to $400 in additional monthly income provides both financial buffer and psychological evidence that you are not helpless in the face of conditions you cannot control.

| ⚠ Watch Out The most damaging recession financial mistakes in the first 30 days: Doing nothing and hoping conditions improve before income is affected. By the time the impact arrives, options are narrower. Withdrawing from retirement accounts early. A $20,000 early withdrawal at age 40 costs $6,000 to $8,000 in penalties and taxes immediately, plus the compounding that $20,000 would have produced over 25 years, which could have exceeded $150,000. Taking on high-interest consumer debt to maintain a pre-recession lifestyle. Source: IRS early withdrawal penalty rules at irs.gov. Federal Reserve SHED Report 2020. |

Category 1: Service Income That Grows in Recessions

The most reliable income during a recession comes from services that address the specific problems recessions create. As unemployment rises, as businesses cut costs and as individuals face financial pressure they have never experienced before, demand for specific help grows dramatically. The strategies in this category are not just recession-resistant. They are often recession-amplified.

| Financial Coaching and Debt Counseling Highest-Demand Recession Service in the US Difficulty: Low to Medium | Speed to Income: 2 to 4 weeks Earning Range: $50 to $150 per hour | $400 to $2,000 per month per ongoing client | Recession Durability: Very High. Demand rises directly with unemployment and financial stress. What it is Financial coaching is the practice of helping individuals and families understand their financial situation, create a realistic budget, build a debt payoff plan and develop the habits that lead to stability. It is distinct from licensed financial advising, which focuses on investment management. Financial coaching focuses on the behavioral and structural aspects of personal finance: helping people understand why they are in their current situation and what specific actions will move them toward recovery. How it works in practice You work with clients one-on-one through video calls, phone or in-person sessions. Each session covers the client’s financial snapshot, progress toward goals, new challenges and specific action steps for the coming period. You do not need a license to offer financial coaching in the United States. You need genuine knowledge of personal finance fundamentals, strong listening skills and the ability to explain concepts clearly to people with no prior financial education. Why it holds up during a recession Demand for financial coaching rises sharply during recessions because the number of Americans facing financial difficulty grows while their ability to pay a traditional financial advisor does not. During the 2020 recession, financial coaching platforms reported a 300 to 400 percent increase in new client inquiries within 90 days of the pandemic-driven downturn, per the Financial Coaching Association of America. How AI makes this more effective: AI tools help financial coaches generate personalized budget templates, debt payoff scenarios and financial education materials in minutes, allowing a coach to serve more clients with higher-quality materials than manual preparation would permit. The honest limitation: Financial coaching is not licensed financial advice. Coaches must be explicit with clients that they are not providing investment advice, tax guidance or legal counsel. Stay within that boundary to protect both parties. Your first step this week: Join the Financial Coaching Association of America at financialcoachingassociation.org to understand the best practices. Offer your first three sessions at a reduced rate to build initial testimonials. Sources: Financial Coaching Association of America at financialcoachingassociation.org. Federal Reserve SHED Report 2020. |

| Home Repair and Maintenance Services Most Consistent Recession Income for Practically Skilled Americans Difficulty: Low (requires practical skills and basic tools) | Speed to Income: 1 to 2 weeks Earning Range: $25 to $75 per hour | $800 to $3,000 per month part-time | Recession Durability: High. People cut professional contractors but still need homes maintained. What it is Home repair and maintenance covers the range of practical tasks homeowners and renters need done but can no longer justify paying full-service contractors to handle during a downturn. Fixing leaky faucets, patching drywall, painting rooms, repairing fences, installing fixtures, cleaning gutters, sealing windows and dozens of similar tasks represent genuine needs that persist regardless of economic conditions. How it works in practice You market through platforms like Thumbtack at thumbtack.com, TaskRabbit at taskrabbit.com and Bark at bark.com, as well as through neighborhood Facebook groups and Nextdoor. You assess the scope of work, provide a clear quote and complete the job. For tasks beyond your skill level, you decline rather than attempting work that could damage property or create liability. Why it holds up during a recession During recessions, demand for affordable skilled tradespeople rises while supply of clients who can afford premium contractors falls. Homeowners who cannot sell in a weak real estate market often choose to repair and improve their homes instead, which increases home maintenance demand precisely when job markets weaken. How AI makes this more effective: AI tools help home repair providers generate professional job estimates and invoices, research material costs for accurate quoting and create targeted marketing content for neighborhood platforms. The honest limitation: Home repair services carry liability risk if work is done incorrectly. Carry general liability insurance before taking on any home repair work. Basic coverage starts at approximately $30 to $50 per month through Next Insurance at nextinsurance.com. Your first step this week: Sign up for Thumbtack at thumbtack.com, create your professional profile listing specific repair categories you are competent in and respond to the first three relevant leads the same day they arrive. Sources: Thumbtack at thumbtack.com. Next Insurance at nextinsurance.com, April 2026. |

| Childcare and Elder Care Services Most Essential and Recession-Resistant Personal Service Difficulty: Low to Medium (background check required) | Speed to Income: 1 to 3 weeks Earning Range: $15 to $35 per hour | $1,000 to $3,000 per month | Recession Durability: Very High. Care for dependents cannot be deferred regardless of economic conditions. What it is Childcare and elder care are among the most genuinely essential services in the American economy because the need for them does not decrease when incomes fall. Parents who lose one income source still need childcare for the other partner to remain employed. Elderly family members who need assistance do not need less care because a recession has reduced family income. Care work is recession-resistant because it addresses a non-discretionary human need. How it works in practice Offer services through Care.com at care.com for both childcare and elder care, and Sittercity at sittercity.com for babysitting and nanny services. Both platforms require a background check that takes one to three business days. Once approved, you respond to family inquiries, conduct meet-and-greet sessions before accepting new clients and build ongoing care relationships that generate recurring weekly income. Why it holds up during a recession The need for care does not correlate with economic conditions but the availability of institutional care does. Daycare centers and professional facilities are expensive, and some families shift to individual care providers who offer competitive rates during recessions. This substitution effect means individual care providers often see demand increase when institutional alternatives become financially out of reach. How AI makes this more effective: AI tools help care providers create professional profiles, generate schedule management systems and draft communication templates for families, improving the quality and professionalism of the service. The honest limitation: Care work involving minor children requires extra diligence in professional behavior and boundary-setting. Always communicate through official platform messaging for early engagements and inform parents immediately of any incidents. Your first step this week: Create a profile on Care.com at care.com. Complete the background check and write a specific, warm profile description that reflects your genuine experience with children or elderly adults. Sources: Care.com at care.com. Sittercity at sittercity.com, April 2026. |

| Grocery Delivery and Essential Errands Fastest Way to Generate Income in Any US City During a Recession Difficulty: Very Low (reliable vehicle or bicycle required) | Speed to Income: 24 to 72 hours Earning Range: $14 to $28 per hour gross | $9 to $18 after vehicle expenses | Recession Durability: High. Essential goods delivery grows as people reduce discretionary outings. What it is Grocery delivery through apps like Instacart, Shipt, DoorDash and Gopuff provides one of the fastest paths from zero to active income for any American with a reliable vehicle. These platforms approve new workers within 24 to 72 hours, have no minimum hour requirements and pay weekly or with instant cash-out options. During a recession, as people reduce discretionary spending and limit unnecessary outings, demand for grocery and essential goods delivery rises rather than falls. How it works in practice After downloading the app and completing a background check, you set your own availability and begin accepting delivery requests. Each request shows the estimated payout before you accept. The most efficient approach is combining two or more delivery apps simultaneously, accepting the best-paying request from whichever platform offers it at any given moment. Our guide on Best Gig Economy Apps for Extra Income in America 2026 at techaifinance.com covers the full multi-platform strategy in detail. Why it holds up during a recession As restaurants reduce hours or close and families cut dining out spending, grocery purchases increase. More groceries purchased means more grocery delivery demand. The recession dynamic that reduces restaurant delivery may actually increase grocery delivery, making this category more stable than food-only delivery. How AI makes this more effective: The free Gridwise app at gridwise.io automatically analyzes your earnings across all platforms, identifies your highest-earning time slots and tracks expenses for taxes simultaneously. The honest limitation: Track every mile using an app like Everlance from day one. The IRS standard mileage deduction of 70 cents per mile for 2026 significantly reduces your tax burden but requires accurate records to claim. Your first step this week: Download Instacart Shopper at instacart.com/shoppers and DoorDash Dasher at dasherapp.com and complete both sign-up processes simultaneously. You can be earning from both within 72 hours. Sources: Gridwise at gridwise.io. IRS mileage rate at irs.gov, 2026. TechAIFinance.com Best Gig Economy Apps for Extra Income in America 2026. |

Category 2: Skill-Based Remote Income

Remote work has become a permanent feature of the US economy. This means Americans with digital skills can access clients in any city regardless of local economic conditions. When your city is suffering economically, your client can be somewhere that is not. Skill-based remote income is the category that most directly reduces your exposure to the specific economic conditions of your geographic location.

| Freelance Writing and Content Creation Most Accessible Skill-Based Remote Income During a Recession Difficulty: Low (clear writing ability required) | Speed to Income: 1 to 3 weeks Earning Range: $25 to $100 per hour | $500 to $4,000 per month | Recession Durability: Medium to High. Content demand remains strong even as budgets tighten. What it is Freelance writing covers the range of written content businesses need: blog posts, website copy, email newsletters, social media content, product descriptions and case studies. During a recession, companies that previously employed full-time content staff often transition to freelance relationships to reduce fixed costs while maintaining content output. This structural shift creates increased demand for freelance writers precisely during periods when full-time content employment becomes scarcer. How it works in practice Find clients through Contently at contently.com for experienced writers seeking brand clients, ClearVoice at clearvoice.com for consistent assignment flow and Vocal Media at vocal.media for building a public portfolio. Pitch or apply for writing assignments, complete them to the brief, submit for review and receive payment on the platform’s schedule. Building a specialty in a high-value topic area such as finance, technology or healthcare significantly increases your per-word rate. Why it holds up during a recession Content is one of the last budget lines smart businesses cut because their online presence continues generating leads regardless of economic conditions. A business that stops publishing during a recession loses search engine visibility that takes months to rebuild. Content budgets are stickier than most marketing spend during downturns, making this a more stable freelance category than many alternatives. How AI makes this more effective: AI writing tools dramatically increase hourly output by handling research, outline generation and first draft structuring. A writer who previously produced 1,500 words of finished content per hour can produce 2,500 to 3,000 words using AI-assisted workflows. The honest limitation: Freelance writing during a recession is competitive because more people with writing skills enter the market when full-time positions disappear. Specializing in a specific industry commands rates that commodity writing cannot, which is the primary differentiator. Your first step this week: Create a free portfolio on Contently at contently.com. Upload three writing samples and publish one high-quality article in your strongest knowledge area on Vocal Media or Medium to establish visible writing history. Sources: Contently at contently.com. ClearVoice at clearvoice.com, April 2026. |

| Online Tutoring and Skills Teaching Best Recession Income for Anyone With Teaching Ability Difficulty: Low (knowledge in a specific subject required) | Speed to Income: 1 to 2 weeks Earning Range: $25 to $100 per hour on platforms like Wyzant | Recession Durability: Very High. Education demand rises sharply as people invest in skills. What it is Online tutoring connects people with knowledge in a specific subject to students who need help in that area. Subjects range from academic topics including math, science and test preparation to professional skills including coding, accounting, marketing and language learning. During a recession, tutoring demand rises because unemployed workers invest in upskilling, students seek academic support when family resources are reduced and professionals pursue certifications that make them more competitive. How it works in practice Create a tutor profile on Wyzant at wyzant.com, which allows you to set your own hourly rate and keep 75 percent of earnings, or Preply at preply.com, which specializes in language and skills instruction with a global student base. Select the subjects you teach, set your availability and rate and respond to student inquiries. Initial sessions with new students convert to ongoing relationships when genuinely helpful, creating recurring weekly income from a single client acquisition effort. Why it holds up during a recession The 2020 recession demonstrated definitively that online tutoring demand is recession-accelerating. Google search volume for online tutoring increased more than 1,000 percent in April 2020 and remained elevated for two years. Recessions create three simultaneous tutoring demand drivers: displaced workers seeking new skills, under-resourced students and parents investing in their children’s outcomes. How AI makes this more effective: AI tools help tutors create customized lesson plans, practice problems and assessment materials in a fraction of manual preparation time. A tutor previously spending 45 minutes preparing per session can prepare the same quality session in 15 minutes using AI-generated materials. The honest limitation: Building an online tutoring income takes several weeks because your initial profile has no reviews. Respond to every student inquiry within one hour during the first 30 days to maximize your conversion rate, and accept first students at a slightly lower rate to build your review foundation. Your first step this week: Create your Wyzant tutor profile at wyzant.com today. Research what other tutors charge for your subject by browsing existing profiles before setting your rate. Sources: Wyzant at wyzant.com. Falcon Digital Marketing search volume analysis 2025. BLS education spending patterns at bls.gov. |

| Virtual Assistant and Remote Administrative Services Most Accessible Remote Income for Organized Americans Difficulty: Low (organizational skills and computer proficiency required) | Speed to Income: 1 to 3 weeks Earning Range: $18 to $45 per hour | $800 to $3,500 per month part-time | Recession Durability: Medium to High. Small businesses cut staff but still need administrative support. What it is A virtual assistant provides remote administrative, organizational and operational support to businesses and executives. Tasks include email management, calendar scheduling, data entry, research, customer service correspondence, social media posting and basic bookkeeping. During a recession, many small businesses that previously employed in-office administrative staff shift to virtual assistants as a cost-saving measure, since virtual assistants can be paid hourly for only the hours worked rather than carrying the overhead of a salaried employee. How it works in practice Find work through Belay at belaysolutions.com, which places US-based virtual assistants with established businesses at professional rates, Time Etc at timeetc.com for executive assistant work, and Fancy Hands at fancyhands.com for task-based work without a fixed schedule commitment. You can also market directly to small businesses through LinkedIn and local business networks. Why it holds up during a recession As businesses reduce full-time staff, remaining employees become overloaded with tasks that still need completing. Outsourcing those tasks to a virtual assistant at a lower cost than a full-time hire is often the most financially rational decision for a business maintaining operations with reduced payroll. This creates counter-cyclical demand precisely when other employment categories are contracting. How AI makes this more effective: AI-assisted virtual assistants handle routine portions of administrative tasks automatically, managing email filtering, calendar optimization and research tasks in roughly half the time required for purely manual execution. The honest limitation: Virtual assistant work requires clear scope agreements before starting. Clients who hire during financial stress sometimes expand scope without increasing pay. Establish clear deliverables, hours and rates in writing before any engagement. Your first step this week: Research Belay at belaysolutions.com and Time Etc at timeetc.com and apply to both this week. While waiting for approval, draft a one-page service description to send directly to small business owners in your network. Sources: Belay at belaysolutions.com. Time Etc at timeetc.com, April 2026. |

Category 3: Asset-Based and Passive Income

One of the most important differences between Americans who navigate recessions successfully and those who do not is the presence or absence of income that does not depend on trading personal time for money. When employment hours are cut or a job disappears, active income stops immediately. Income from assets, digital products and passive income streams continues regardless of employment status.

| Renting Assets You Already Own Fastest Passive Income Activation During a Recession Difficulty: Very Low (requires an eligible asset: car, space or equipment) | Speed to Income: 1 to 5 days Earning Range: $50 to $1,500 per month depending on asset type | Recession Durability: Medium. Asset rental demand varies by category during recessions. What it is Americans own assets that can generate income when not in use. A car that sits in the driveway earns nothing. A spare room, garage, basement, parking space or storage area produces nothing while empty. Photography equipment, tools, musical instruments and recreational gear all represent capital that can generate cash flow. Platforms that connect asset owners with people who need temporary access have made this monetization genuinely practical. How it works in practice Primary asset rental platforms include Turo at turo.com for cars, earning $400 to $1,200 per month in active markets. Neighbor at neighbor.com for unused storage space, earning $50 to $500 per month. Getaround at getaround.com for cars with connected device technology eliminating key exchange. Fat Llama at fatllama.com for equipment including cameras, tools and electronics. Listing across relevant platforms takes a few hours of initial setup and then generates passive income with minimal ongoing effort. Why it holds up during a recession uring recessions, storage rental tends to increase as people downsize living situations and need places to store belongings. Equipment rental tends to increase as people pursue DIY projects they previously paid professionals to handle. Diversifying across multiple asset types provides more stable total rental income than depending on a single category. How AI makes this more effective: AI tools help asset owners write compelling listing descriptions, set competitive pricing based on comparable listings and respond to inquiries professionally. Quick response times are among the strongest predictors of listing success on peer-to-peer rental platforms. The honest limitation: Not all assets qualify for peer-to-peer rental. Cars must meet age and condition requirements that vary by platform. Space rental may be subject to lease restrictions or HOA rules. Review your lease, HOA rules and insurance policy before listing any asset. Your first step this week: Review your most valuable idle assets: your car, unused spaces and significant equipment. Check whether each qualifies on the relevant platform and set up your first listing this weekend. Sources: Turo at turo.com. Neighbor at neighbor.com. Fat Llama at fatllama.com, April 2026. |

| Selling Digital Products and Templates Best Recession-Proof Passive Income for Knowledge Workers Difficulty: Medium (requires expertise and time to create) | Speed to Income: 1 to 4 weeks with an existing audience Earning Range: $200 to $5,000 per month with an established catalog | Recession Durability: High. Digital products require no inventory and generate income regardless of economic conditions. What it is Digital products are downloadable files or online-delivered content that customers purchase and receive instantly. Unlike physical products, which require inventory and shipping, digital products have zero additional production cost per sale. During a recession, the most relevant categories shift to match what people need: resume templates, budget planners, debt payoff calculators, job application frameworks and DIY instructional content all attract buyers navigating reduced income for the first time. How it works in practice Create a product that solves a specific problem for a specific audience. List it on Gumroad at gumroad.com, Teachable at teachable.com or your own website. When a customer purchases, they receive instant digital access. The platform handles payment processing, delivery and refund management. Once created, the product earns indefinitely from a single creation effort. Why it holds up during a recession Digital products scale infinitely at zero marginal cost. The same financial planning spreadsheet created during a recession sells to a buyer in Texas, Florida and Ohio all in the same hour with no additional effort. Creating products that directly address recession-specific problems, such as budget templates or debt payoff trackers, aligns your product offering with the exact problems creating the highest demand during a downturn. How AI makes this more effective: AI tools have reduced digital product creation time dramatically. A product that took 40 hours to create manually in 2022 can be created in 15 to 20 hours in 2026 using AI-assisted workflows for outlines, structure, visuals and copy. The honest limitation: Digital product income requires an audience or distribution channel to generate initial sales. Creating an excellent product with no way to reach potential buyers produces no income. Use Gumroad’s internal discovery marketplace or Etsy’s organic search if you do not yet have an existing audience. Your first step this week: Identify the single most painful problem people in your professional area are facing during this recession. Create one digital product that solves it. List it on Gumroad at gumroad.com at $9 to $29 to maximize initial sales and build your first reviews. Sources: Gumroad at gumroad.com. TechAIFinance.com How to Make Passive Income in the US 2026. |

| High Yield Savings and Treasury Bills Safest Way to Make Your Cash Work During a Recession Difficulty: Very Low (30 minutes of setup) | Speed to Income: First interest within 30 days Earning Range: $40 to $400 per month per $10,000 to $100,000 in savings | Recession Durability: Very High. Interest income is unaffected by recession economic conditions. What it is During a recession, when job security is reduced and investment markets are uncertain, the cash you hold is your most important resource. Most Americans hold that cash in accounts paying 0.1 to 0.5 percent annual interest. Moving the same cash to a high yield savings account or Treasury bills paying 4 to 5 percent annually does not require any additional risk, does not lock up the money for a long period and does not require financial expertise. It requires only the decision to move it and 30 minutes of online account setup. How it works in practice A high yield savings account at an online bank pays significantly more interest than a traditional bank account while maintaining full FDIC insurance up to $250,000 per depositor. Treasury bills purchased through TreasuryDirect at treasurydirect.gov pay similar or slightly higher rates with US government backing and mature in four to 52 weeks, keeping capital accessible on a short-term basis. During a recession, this combination of safety, liquidity and above-average yield is the most rational place to hold the cash reserves serving as your financial safety net. Why it holds up during a recession Recessions are often preceded by Federal Reserve interest rate increases designed to slow inflation, which means high yield savings rates are frequently at elevated levels precisely as economic conditions deteriorate. The interest income generated is independent of stock market performance, business conditions or employment trends. A $50,000 emergency fund earning 4.8 percent annually generates $2,400 per year in completely passive interest income regardless of what happens in the broader economy. How AI makes this more effective: AI financial comparison tools identify the current highest-yielding accounts across all major online banks in seconds, ensuring you always capture the best available rate without manual research. The honest limitation: If the Fed begins cutting interest rates significantly, high yield savings and Treasury bill rates will fall. These are appropriate for short to medium-term cash reserves rather than long-term wealth building. Your first step this week: Check your current savings account interest rate. If it is below 4 percent, open a high yield savings account using our guide at techaifinance.com/best-high-yield-savings-accounts-us-2026. Sources: FDIC rate data at fdic.gov. TreasuryDirect at treasurydirect.gov. TechAIFinance.com Best High Yield Savings Accounts in the US 2026. |

Category 4: Recession Investment Opportunities

Recessions create genuine investment opportunities that do not exist during periods of economic expansion. Asset prices fall across multiple categories, sometimes to levels that represent exceptional long-term value for investors with the capital and discipline to buy while fear drives most participants to sell. This is not advice to invest recklessly. It is an observation that the Americans who invest during recessions, when they can afford to without endangering essential reserves, often experience their best investment outcomes.

| Investing in Recession-Period Market Declines The Historically Highest-Return Activity Available During a Recession Difficulty: Low (requires capital beyond emergency reserves) | Speed to Income: Returns realized over 12 to 60 months Earning Range: Historically above-average returns over 5 to 10 year holding periods | Recession Durability: Long-term positive. Short-term volatile. What it is Every major US stock market decline in the past century has eventually been followed by a recovery to new highs. An investor who purchased shares of a broad US stock market index fund during the depths of every recession since 1950 and held for five or more years has never experienced a negative return over that holding period, based on historical S&P 500 data. This historical pattern does not guarantee future results but establishes that investing in low-cost diversified index funds during downturns has been one of the most consistently rewarding financial decisions for Americans with a long time horizon. How it works in practice When markets fall during a recession, the same investment that previously cost $100 now costs $70 or $50. If the long-term trajectory of the US economy continues upward, as it has through every previous recession, those shares purchased at $70 or $50 will eventually be worth more than they were before. An investor who put $10,000 into the S&P 500 in March 2009 during the financial crisis saw that investment exceed $50,000 by 2019, a 400 percent gain over ten years from money invested when fear was at its peak. Why it holds up during a recession The counter-cyclical nature of recession investing is its defining characteristic. Almost every other strategy in this guide generates more income because recession conditions create more demand. Investing does the opposite: recession conditions reduce asset prices, which creates more value per dollar invested. The two activities are complementary: the income generated through other strategies in this guide provides the capital that recession-period investing requires. How AI makes this more effective: AI financial planning tools help investors model the long-term impact of investing specific amounts during a market decline at various assumed recovery timelines, providing a concrete framework for evaluating the opportunity rather than making emotional decisions during a stressful period. The honest limitation: Recession investing requires capital that is genuinely beyond your emergency fund and that you can afford to have temporarily reduced further before recovering. Never invest emergency funds or money earmarked for near-term expenses regardless of market conditions. Your first step this week: If your emergency fund is fully funded at three to six months of expenses and essential income is secured, open a brokerage account at Fidelity or Schwab and set up automatic monthly investments to a total market index fund during any period when markets are meaningfully below recent highs. Sources: S&P 500 historical return data at spglobal.com. Federal Reserve household wealth recovery data at federalreserve.gov. |

| I Bonds and TIPS for Inflation Protection Best Government-Backed Inflation Protection During Economic Uncertainty Difficulty: Very Low (TreasuryDirect account setup required) | Speed to Income: Interest accrual begins immediately Earning Range: Variable rate tied to inflation, recently 3.5 to 9.6 percent | Recession Durability: Very High. Government-backed with no default risk. What it is Series I Savings Bonds are US government savings bonds whose interest rate is tied to the inflation rate. They pay a fixed rate plus an inflation adjustment updated every six months based on the Consumer Price Index. During periods of elevated inflation that frequently accompany government recession-fighting policy responses including stimulus spending, I Bonds pay substantially above-market rates while maintaining complete US government backing with no risk of principal loss. Treasury Inflation-Protected Securities, called TIPS, are similar inflation-linked bonds available in longer maturities. How it works in practice You purchase I Bonds directly through TreasuryDirect at treasurydirect.gov. The purchase limit is $10,000 per Social Security number per calendar year, plus an additional $5,000 using your federal tax refund for paper I Bonds. I Bonds must be held for at least one year before redemption and incur a three-month interest penalty if redeemed before five years. Interest is exempt from state and local income tax and federal tax can be deferred until redemption, providing a tax efficiency advantage over high yield savings accounts. Why it holds up during a recession Bonds are valuable during recessionary periods for three reasons. Government stimulus spending during recessions often triggers inflation in the months and years that follow, increasing I Bond rates precisely when they are most in demand. The absolute safety of US government backing provides zero counterparty risk when bank failures and financial stress are more common. The tax deferral on I Bond interest allows earnings to compound at the full pre-tax rate until you choose to recognize the income. How AI makes this more effective: AI tax planning tools help I Bond holders calculate optimal redemption timing from a tax perspective, since the choice of when to redeem affects which tax year the interest income is recognized, which can meaningfully affect your overall tax liability. The honest limitation: I Bonds have a $10,000 annual purchase limit per Social Security number, which limits the total amount you can invest in any single year. They also have a minimum one-year holding period, making them inappropriate for money you might need within 12 months. Your first step this week: Visit TreasuryDirect at treasurydirect.gov, create a free account and check the current I Bond composite rate. If the rate exceeds what your high yield savings account pays, purchase the maximum $10,000 allocation this calendar year. Sources: TreasuryDirect I Bond rates at treasurydirect.gov, April 2026. IRS I Bond tax treatment at irs.gov. BLS Consumer Price Index at bls.gov. |

How to Cut Expenses Without Cutting Your Life

Generating additional income is one half of recession financial resilience. The other half is protecting what you already earn by eliminating waste strategically without making life feel punishing.

The spending hierarchy for recession periods

Tier 1: Non-negotiable

Housing payments, utilities, basic food, essential transportation, health insurance and necessary medications. Cutting any of these creates downstream consequences that cost more to resolve than the savings they generate.

Tier 2: Reduce but do not eliminate

Grocery spending can be reduced 15 to 25 percent through meal planning and reducing food waste. Transportation costs can often be reduced by combining errands or shifting to more fuel-efficient habits. Internet and phone plans can frequently be negotiated lower by calling and asking directly.

Tier 3: Pause and evaluate

Streaming subscriptions, gym memberships, dining out, travel and clothing beyond necessities can be paused without immediate life quality impact and restarted when income is stable. Conduct a full subscription audit: list every recurring monthly charge and cancel every one you cannot justify during reduced income.

| 💡 Pro Tip The fastest legal way to reduce a bill you are already paying is to call the company and ask. Internet providers, cell phone carriers, insurance companies and credit card issuers all have retention offers for customers considering canceling. These offers are almost never advertised. A 30-minute phone call to your internet provider, cell carrier and one insurance company has a realistic expected value of $50 to $150 per month in reduced bills for most American households. Call during business hours, be polite and direct. Say specifically: I am looking to reduce my monthly costs and considering alternatives. What can you do for me? |

Recession-Proofing Your Income for the Long Term

The strategies in this guide are most useful implemented before a recession rather than during one. The Americans who weather economic downturns most successfully built diversified income, maintained savings and developed marketable skills during preceding periods of relative stability.

Build an emergency fund of six months of expenses

The single most impactful financial buffer against recession hardship is a fully funded emergency fund held in a high yield savings account. Six months provides genuine resilience: enough time to replace a lost income, pivot to a new strategy or wait out the worst of a downturn without emergency decisions driven by immediate desperation.

Develop at least two income streams before you need them

Any second income stream, no matter how modest, changes your financial risk profile fundamentally. An employee with a side income of $500 per month has a meaningfully different experience of a layoff than one with no alternative. That $500 provides time: to find a new position without accepting the first offer out of desperation, to develop the side income further, to evaluate the situation calmly rather than from a position of immediate crisis.

Invest in skills that are recession-resistant

The skills that command strong income during recessions help people navigate financial difficulty, are genuinely essential regardless of economic conditions and can be delivered remotely. Financial literacy, healthcare skills, technical problem-solving, teaching ability and practical repair skills all fall into this category. Investing in one of these skill areas before a recession begins is the most durable preparation available.

Full Strategy Comparison Table

| Strategy | Category | Earning Range | Speed | Recession Durability |

| Financial Coaching | Service | $50-150/hr | 2-4 weeks | Very High |

| Home Repair | Service | $25-75/hr | 1-2 weeks | High |

| Childcare and Elder Care | Service | $15-35/hr | 1-3 weeks | Very High |

| Grocery Delivery | Service | $14-28/hr gross | 24-72 hours | High |

| Freelance Writing | Remote Skill | $25-100/hr | 1-3 weeks | Medium to High |

| Online Tutoring | Remote Skill | $25-100/hr | 1-2 weeks | Very High |

| Virtual Assistant | Remote Skill | $18-45/hr | 1-3 weeks | Medium to High |

| Asset Rental | Passive | $50-1,500/mo | 1-5 days | Medium |

| Digital Products | Passive | $200-5,000/mo | 1-4 weeks | High |

| High Yield Savings | Passive | $40-400/mo per $10-100K | 30 days | Very High |

| Market Investing | Investment | Above-avg long-term | 12-60 months | Long-term positive |

| I Bonds and TIPS | Investment | Inflation-adjusted | Immediate accrual | Very High |

| 💡 Real-World Example Consider a hypothetical 42-year-old project manager in Detroit named Robert, laid off in month two of a recession when his employer eliminated his department. Week 1: Robert mapped his exact financial position. He had $18,000 in savings earning 0.3 percent, $4,200 in checking and $67,000 in a 401k. Monthly expenses were $4,100. His wife earned $1,800 per month part-time. He had 55 days of expenses in accessible cash. Week 2: He moved his savings to a high yield account earning 4.7 percent, generating an additional $71 per month immediately. He negotiated combined monthly savings of $87 from his internet provider and cell carrier. He canceled four streaming services saving $52 per month. Week 3: He signed up for Thumbtack highlighting his practical home repair skills. He received his first booking within six days: a fence repair at $180. Month 2: His home repair work generated $1,100 per month. He began a part-time virtual assistant engagement at $28 per hour for 12 hours per week, adding $1,344 per month. Month 4: Combined income from his wife, Thumbtack, virtual assistant work and savings interest totaled $4,380 per month, slightly above household expenses. He began investing $500 per month into a broad index fund at a market level 28 percent below its previous peak. Month 9: Robert accepted a new full-time role at a comparable salary. He kept his Thumbtack and virtual assistant work at reduced hours generating $800 per month supplemental income. His recession-period index fund investments had already recovered 19 percent in value. This example is illustrative. Actual outcomes depend on individual skills, market conditions and effort. |

Frequently Asked Questions

Which income strategies work fastest when I have just lost my job?

Grocery delivery through Instacart or DoorDash generates income within 24 to 72 hours. Asset rental through Turo or Neighbor can generate income within days of listing. Virtual assistant work typically takes one to three weeks for approval. Home repair through Thumbtack can generate a first booking within one to two weeks. Start with the fastest-activating strategies first while simultaneously pursuing the ones that take longer but produce higher rates per hour.

Should I withdraw from my 401k during a recession?

In almost every circumstance, no. Early withdrawal before age 59 and a half incurs a 10 percent penalty plus income tax at your regular rate, together reducing a $20,000 withdrawal to approximately $12,000 to $14,000. Additionally, withdrawing during a recession means selling at depressed prices and permanently removing capital from the compounding that will occur when markets recover. Exhaust all other options including cutting expenses, generating additional income and accessing unemployment benefits before considering retirement account withdrawal.

How do I apply for unemployment benefits in the US?

Unemployment benefits are administered at the state level. Apply through your state’s official unemployment insurance website, which you can find through the US Department of Labor’s CareerOneStop portal at careeronestop.org. Apply in the first week after your last day of work. Benefits accumulate only after your application is approved and most states impose a one-week waiting period before benefits begin.

What government assistance programs are available during a recession?

- SNAP Food Assistance: food assistance for Americans with income below certain thresholds. Opens in new tab.

- Medicaid: free or low-cost health insurance for Americans below program income thresholds. Opens in new tab.

- LIHEAP Energy Assistance: federal assistance with heating and cooling bills for income-eligible households. Opens in new tab.

- 211.org: connects Americans with local social services including food banks, housing assistance and employment resources. Opens in new tab.

| ⭐ Key Takeaway A recession does not have to set your financial life back. For Americans who respond quickly and strategically, it can accelerate financial progress. The income strategies in this guide generate real money. The investment opportunities a recession creates are genuine. The expense reductions available through negotiation are accessible to almost every American household. The difference between financial resilience and financial crisis during a recession is almost always preparation and response speed, not income level or luck. Start today. Not when the recession gets worse. Not when your income is affected. Today, while you have the time and energy to build the systems that will protect you if it does. |

Conclusion

Twelve strategies for making money during a recession, from financial coaching that grows in demand as economic stress rises, to asset rental that monetizes what you already own, to I Bonds that protect your cash with zero risk. Some generate income within days. Others build over months. Together they represent the range of options available to Americans at every income level when economic conditions tighten.

The Americans who emerge from recessions in a stronger financial position are the ones who acted on both sides of the equation simultaneously: generating additional income while cutting unnecessary spending, and channeling the margin into assets that compound over time. That combination is available to any American willing to execute it.

For Americans who want to build income sources durable beyond any single recession, our guide on how to build generational wealth in the US covers the seven pillars of long-term family wealth. For the full range of income platforms across normal and difficult conditions, our guide on best side hustles for Americans in 2026 covers 20 platforms across every skill level.

| 📥 Free Download: Recession Survival and Income Toolkit 2026 A practical toolkit: 30-day emergency checklist, recession budget template and income diversification tracker. Free. Email required. For informational purposes only. |

| 📲 Share This Guide If this guide helped you think more clearly about your financial options during a difficult economic period, share it with someone who needs it right now. Share on WhatsApp, Facebook or by text message. Thank you for reading TechAIFinance.com. |

Read Next

Continue building your financial resilience on TechAIFinance.com:

- How to Build Generational Wealth in the US

- How to Make Passive Income in the US 2026

- Best High Yield Savings Accounts in the US 2026

- Best Gig Economy Apps for Extra Income in America 2026

- Best Side Hustles for Americans in 2026

| ✍ About the Author Written by: TechAIFinance Editorial Team Edited and Fact-Checked by: Olayinka Adejugbe Olayinka Adejugbe is not a licensed financial advisor. The content on TechAIFinance.com is produced for educational purposes only and should not be treated as personalized financial advice. Olayinka is the founder and lead editor of TechAIFinance.com. He holds a Global Certification in Artificial Intelligence and Applied Innovation and an Award of Completion in Behavioral Counseling from the World Health Organization. With a strong working knowledge of personal finance and accounting principles, Olayinka oversees the editorial review of every article on this site to ensure accuracy, currency and practical usefulness. Every article on TechAIFinance.com is produced by our research team and reviewed by Olayinka before publication. We verify statistics against named authoritative sources and update content when circumstances change. Visit our About page to learn more about our editorial process. Use our Contact page to get in touch. |

Important Disclaimer

The content published on TechAIFinance.com is for educational and informational purposes only. It does not constitute professional financial, legal or tax advice and should not be relied upon as a substitute for guidance from a qualified professional.

Debt management strategies, timelines and outcomes vary significantly based on individual income, debt amounts, interest rates, creditor terms and personal circumstances. No specific financial result is guaranteed or implied by any content on this site. Always consult a qualified financial advisor, credit counselor or attorney before making significant financial decisions. Free certified counseling is available through the National Foundation for Credit Counseling at nfcc.org.