| Content Note This guide provides general information about medical bill negotiation strategies available to Americans. It is not legal, medical or financial advice. Medical billing practices, hospital financial assistance policies and collection laws vary by state and by provider. Always verify specific details with the billing department and consult a patient advocate or attorney for complex billing disputes. All statistics cited were verified in April 2026. |

Most Americans who receive a medical bill do one of two things: they pay it immediately without question or they ignore it out of anxiety and hope it goes away. Both responses leave money on the table that most patients are legally and practically entitled to recover through negotiation, error correction or financial assistance programs that hospitals are legally required to have but are under no obligation to tell you about proactively.

The medical billing system in the United States is not designed for transparency. The amount on your bill is not necessarily the amount the hospital expects to collect. It is frequently not the amount other patients pay for the same service. It is almost certainly not the amount your insurance company’s negotiated rate would have been. And it may not even be accurate, since studies consistently find billing errors in a significant percentage of hospital bills.

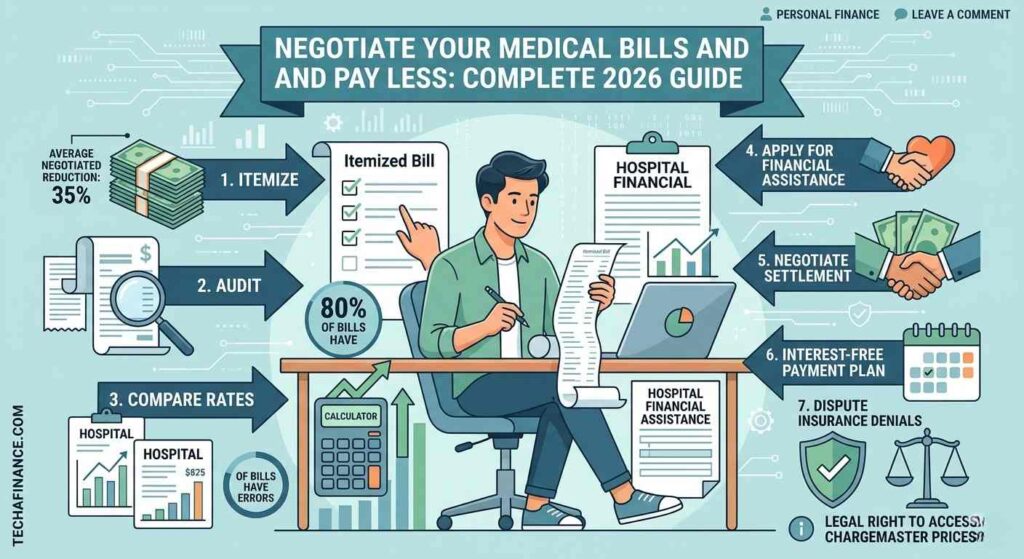

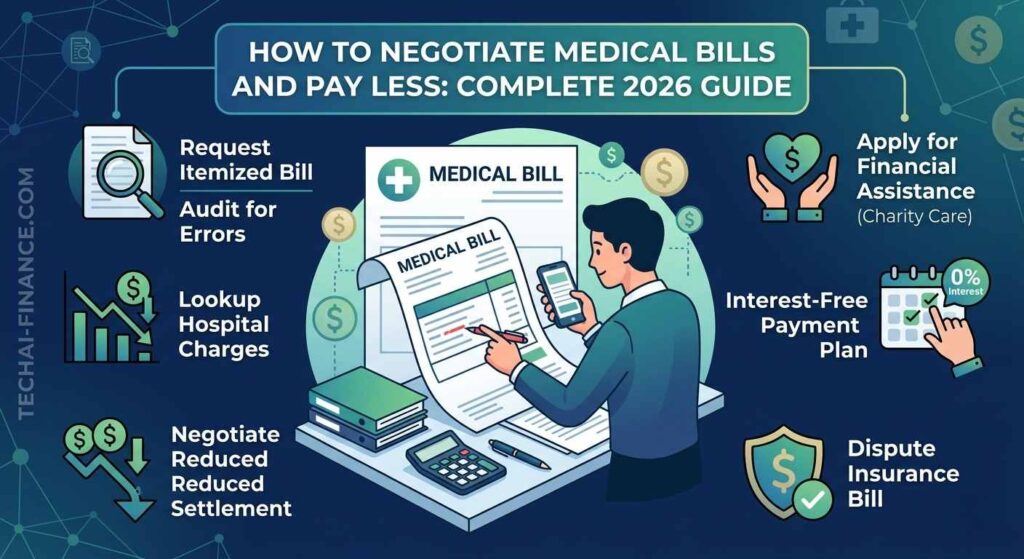

This guide covers every tool available to Americans for reducing medical bills legally and ethically: auditing your bill for errors, understanding what the hospital actually charges other payers, applying for hospital financial assistance, negotiating a reduced settlement, setting up an interest-free payment plan and disputing bills that should have been covered by insurance. Every section includes the specific language to use in conversations with billing departments, because knowing what to say matters as much as knowing what you are entitled to ask for.

This guide was written by Olayinka Adejugbe, founder of TechAIFinance.com and holder of a Global Certification in Artificial Intelligence and Applied Innovation.

| ℹ Quick Summary Medical billing in the US in 2026: the numbers that matter Americans carry approximately $195 billion in medical debt as of 2025, making it the most common form of debt in collections in the United States, per the Consumer Financial Protection Bureau 2025 Medical Debt Report. A 2023 study by medical billing auditor Medliminal found billing errors in approximately 80 percent of medical bills reviewed, with the average error amounting to $1,300 per bill. Hospitals that receive federal funding are legally required under the Affordable Care Act to have charity care and financial assistance programs, but only 60 percent of eligible patients who could qualify apply, per the American Hospital Association 2025. Americans who negotiate medical bills directly with providers reduce their bills by an average of 35 percent, per a 2024 study by the nonprofit Patient Advocate Foundation. A 2022 federal rule now requires hospitals to post their chargemaster prices and negotiated insurance rates publicly, giving patients the legal right to access what other payers are charged for the same services. Sources: CFPB Medical Debt Report 2025. Medliminal billing audit data 2023. American Hospital Association 2025. Patient Advocate Foundation 2024 study. |

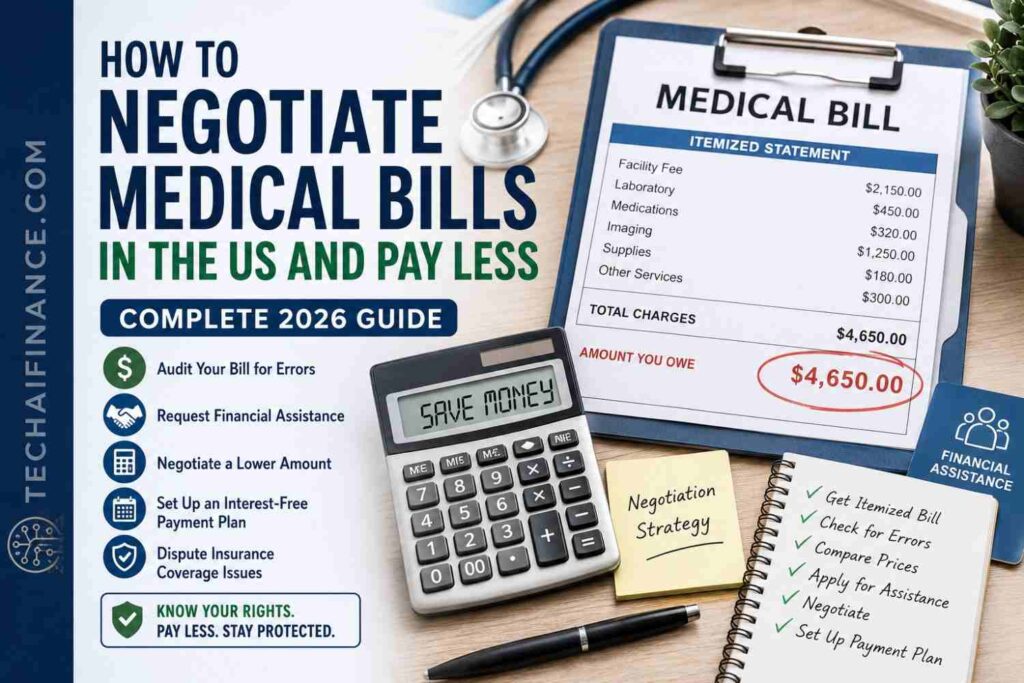

| 📘 What This Guide Covers In this guide you will find: Step 1: How to get an itemized bill and why you must always request one Step 2: How to audit your medical bill for the most common billing errors Step 3: How to look up what your hospital charges and what your insurance should have paid Step 4: How to apply for hospital charity care and financial assistance Step 5: How to negotiate a reduced lump-sum settlement Step 6: How to set up an interest-free payment plan Step 7: How to dispute a bill that should have been covered by insurance Word-for-word phone scripts for every negotiation scenario What to do about medical debt in collections How AI tools help you negotiate medical bills faster |

Table of Contents

- Why Medical Bills Are Negotiable: The Foundation You Must Understand

- Step 1: Request Your Itemized Bill Immediately

- Step 2: Audit Your Bill for Errors

- Step 3: Look Up What Others Actually Pay for Your Services

- Step 4: Apply for Hospital Financial Assistance Before Paying Anything

- Step 5: Negotiate a Reduced Lump-Sum Settlement

- Step 6: Set Up an Interest-Free Payment Plan

- Step 7: Dispute Bills That Should Have Been Covered by Insurance

- Medical Debt in Collections: What You Can and Cannot Do

- How AI Tools Help You Negotiate Medical Bills

- Frequently Asked Questions

Why Medical Bills Are Negotiable: The Foundation You Must Understand

The most important thing to understand about medical billing in America is that the number on your bill is not a fixed price in any meaningful economic sense. It is a starting number in a system where almost every payer, from major insurance companies to government programs to individual patients, pays a different amount for the same service.

The chargemaster: why the sticker price means almost nothing

Every hospital maintains a chargemaster, which is a master list of the standard prices for every service, procedure and supply the hospital provides. The chargemaster prices are typically two to four times what any major payer actually pays. Medicare pays approximately 90 cents on the dollar relative to hospital costs. Medicaid pays even less in most states. Commercial insurance companies negotiate rates that are typically 20 to 60 percent below chargemaster prices. The only patients who are typically billed at or near chargemaster prices are uninsured patients who do not know to negotiate, which represents one of the most significant inequities in the American healthcare system.

The 2022 Hospital Price Transparency Rule

A federal rule that went into effect in January 2021 and was strengthened with additional enforcement in 2022 requires hospitals to publicly post their chargemaster prices and their negotiated rates with insurance companies for at least 300 shoppable services. The Centers for Medicare and Medicaid Services published this rule to give patients access to pricing information that was previously hidden. This means you now have a legal right to see what your hospital charges Medicare, what it charges your specific insurance company and what it charges other commercial payers for the same procedure before or after receiving care. This information gives you a reference point for negotiation that was not available to patients even five years ago.

Hospitals negotiate with every major payer

If your hospital negotiates rates with Blue Cross Blue Shield, Aetna, Cigna and Medicare, all of which pay below chargemaster prices, there is no logical basis for the hospital to insist that an uninsured or underinsured individual patient must pay chargemaster rates. The hospital’s cost structure and financial sustainability are built around the blend of rates it receives across all payers, not around collecting chargemaster prices from every patient. This is the factual foundation that makes medical bill negotiation legitimate: you are not asking for a special favor when you negotiate. You are asking to pay a rate comparable to what the hospital already accepts from other payers for the same service.

| ⭐ Key Takeaway Never pay a medical bill immediately upon receiving it. Take these steps first: request the itemized bill, audit it for errors, look up the hospital’s posted prices, check whether you qualify for financial assistance and then negotiate from a position of information. Americans who follow this sequence reduce their medical bills by an average of 35 percent according to the Patient Advocate Foundation. That average applies across all income levels, not just low-income households. The hospital billing department expects you to call. They have trained staff whose job is to work through exactly these conversations. |

Step 1: Request Your Itemized Bill Immediately

The summary bill you receive from a hospital or healthcare provider after care is not your complete bill. It is a summary showing total charges by category without the detail needed to identify errors or verify accuracy. You have the right to request a fully itemized bill that lists every individual charge, the specific procedure code for each service, the date each service was delivered and the unit cost for each supply or medication used.

How to request your itemized bill

Call the hospital or provider’s billing department and use the following language:

| 🗣 Script: What to Say I would like to request a complete itemized bill for my account number [your account number]. I need the bill to include every line item with the specific CPT or procedure code, the date of service, the quantity and the individual charge for each item. Please send it to me in writing by mail or email. I need this before I can process any payment. |

CPT codes are the Current Procedural Terminology codes that identify every medical service and procedure in the US billing system. Having the CPT codes allows you to look up exactly what was billed and compare it to what was delivered, which is how billing errors are identified. Most billing departments provide itemized bills within five to ten business days of your request. Do not pay any amount on a summary bill before receiving and reviewing the itemized version.

Step 2: Audit Your Bill for Errors

Medical billing errors are extraordinarily common. Auditing firm Medliminal reviewed thousands of hospital bills and found errors in approximately 80 percent of them. These are not trivial discrepancies. The most common errors involve double billing for the same service, charges for services that were ordered but never delivered, upcoding where a more expensive procedure code is used than the service that was actually performed, unbundling where services that should be billed together as a package are broken apart and billed individually at higher combined cost, and charges for supplies at retail prices rather than the volume-discounted prices hospitals actually pay.

The most common billing errors to look for

- Duplicate charges: Look for the same service billed twice on the same or adjacent dates. Medication administration fees, lab fees and room charges are the most common duplicate charge categories.

- Services not received: Compare the itemized bill against any notes you kept during your care, your discharge summary and your medical records. If you see charges for procedures, consultations or tests you do not recall receiving, request documentation confirming the service was delivered.

- Upcoding: An emergency room visit has five possible billing levels from Level 1 for a minor issue to Level 5 for a complex emergency. If your bill shows a Level 5 ER visit for a condition that was straightforward, ask for documentation supporting that complexity level.

- Unbundling: Certain services have bundled CPT codes that should be billed as a single package. If your itemized bill shows multiple individual codes for components of a service that should be bundled, that is a potential error worth questioning.

- Operating room time overcharges: OR time is billed by the minute in most hospitals. If the billed OR time significantly exceeds the documented surgical time in your records, request the OR log.

- Medication pricing: Check that medications are billed at the hospital’s actual cost rather than the retail pharmacy price. A single dose of a common drug should not appear at a markup of 1,000 percent over the hospital’s acquisition cost.

How to dispute an error you identify

When you identify a potential billing error, do not pay the disputed amount. Call the billing department and explain what you found. Use this language:

| 🗣 Script: What to Say I have reviewed my itemized bill and I believe there is an error on line [line number]. The charge is for [service description or CPT code] on [date]. I do not believe this service was delivered based on my medical records. I am requesting documentation confirming this service was provided before I can include it in my payment. Can you connect me with your billing compliance department or patient advocate? |

If the billing department cannot provide documentation supporting the charge, ask them to remove it from your balance. If they insist the charge is correct and you believe it is not, request a formal billing review. Most hospitals have a formal dispute process and an internal patient advocate whose role is to resolve exactly these situations. If the internal process does not resolve the dispute, you can file a complaint with your state’s hospital licensing authority or, for Medicare and Medicaid patients, with the Centers for Medicare and Medicaid Services.

Step 3: Look Up What Others Actually Pay for Your Services

One of the most powerful negotiating tools now available to American patients is the publicly available hospital pricing data that hospitals are required to post under the 2022 federal price transparency rule. This data shows you exactly what your hospital charges different payers for the same service, giving you a concrete reference point for negotiation.

How to access hospital price data

- The hospital’s own price transparency page: Every hospital covered by the rule must post a machine-readable file with all service prices and a consumer-friendly display of at least 300 shoppable services. Visit the hospital’s website and search for Price Transparency or visit cms.gov/hospital-price-transparency for the CMS database of hospital price files.

- Healthcare Bluebook (healthcarebluebook.com): A free consumer tool that shows fair market prices for hundreds of medical procedures in your geographic area, based on what payers actually pay for those services.

- FAIR Health Consumer (fairhealthconsumer.org): A nonprofit database that shows the typical charges and typical allowed amounts for medical procedures by CPT code in your zip code area.

- Medicare payment lookup: Medicare’s publicly available payment rates for every procedure are the baseline below which no legitimate argument for higher individual patient rates can be made. If Medicare pays $800 for your procedure, paying $3,000 as an uninsured patient is not a market rate. It is a starting point for negotiation.

How to use the price data in your negotiation

When you call to negotiate, reference the data directly:

| 🗣 Script: What to Say I have reviewed the price transparency data your hospital is required to publish under the federal Hospital Price Transparency Rule. For CPT code [code], I can see that your negotiated rate with [insurance company] is [amount]. I would like to settle my balance at a comparable rate. I am prepared to pay [amount] as a lump-sum payment to resolve this account. Alternatively: I checked the Medicare payment rate for this procedure, which is [amount]. I would like to request that my bill be adjusted to the Medicare rate, which is consistent with your established cost-recovery pricing. |

Step 4: Apply for Hospital Financial Assistance Before Paying Anything

Every hospital that receives federal Medicare and Medicaid funding is legally required under the Affordable Care Act to have a financial assistance program, sometimes called charity care, that provides free or reduced-cost care to patients who meet income eligibility requirements. What the law does not require is that hospitals proactively tell you this program exists or help you apply for it.

Who qualifies for hospital financial assistance

Eligibility requirements vary by hospital but are typically based on your household income as a percentage of the federal poverty level. Many hospital financial assistance programs cover patients with income up to 200 to 300 percent of the federal poverty level for free or deeply discounted care, with sliding scale discounts extending further up the income scale. In 2026, 200 percent of the federal poverty level for a family of four is approximately $62,400 per year. A middle-income family with a large medical bill is often surprised to discover they qualify for meaningful financial assistance they never knew existed.

How to apply for financial assistance

Call the hospital billing department or visit the patient financial services office and ask directly:

| 🗣 Script: What to Say I would like to apply for your financial assistance or charity care program. Can you send me the application and the income documentation requirements? I understand the hospital is required to have this program under the Affordable Care Act. I would like to apply before making any payment on this account. |

The application typically requires documentation of your household income, which may include recent tax returns, pay stubs or bank statements. The review process takes one to four weeks at most hospitals. Do not pay your bill while the financial assistance application is pending. If you are approved, the hospital adjusts your balance to the assisted rate before you pay anything.

The ACA income-based billing limitation

The ACA also limits what nonprofit hospitals can charge patients who qualify for financial assistance but did not apply or did not know about the program. Nonprofit hospitals are prohibited from billing financial-assistance-eligible patients more than the amount generally billed to insured patients for the same services, and from engaging in extraordinary collection actions such as lawsuits or reporting to credit bureaus before making reasonable efforts to determine whether the patient qualifies for financial assistance. If you receive a collection notice from a nonprofit hospital for a bill you believe you may have qualified for assistance on, contact the hospital’s financial assistance office immediately.

| ⚠ Watch Out Do not ignore a medical bill even if you cannot pay it. Ignoring a medical bill does not make it go away. After a period that varies by state and hospital, unpaid medical bills can be sent to collections, which can result in the account appearing on your credit report and potential legal action. The No Surprises Act, which took effect in 2022, prohibits surprise billing for emergency care and for out-of-network care at in-network facilities without advance consent, but it does not eliminate all unexpected medical costs. Always review your Explanation of Benefits from your insurer and compare it to the provider’s bill to identify any discrepancy before paying. Source: No Surprises Act effective January 1 2022, summarized at cms.gov/nosurprises. |

Step 5: Negotiate a Reduced Lump-Sum Settlement

After auditing your bill for errors, looking up what other payers are charged and checking whether you qualify for financial assistance, you are in the strongest possible position to negotiate a reduced lump-sum settlement on the remaining balance. Hospitals and providers accept lump-sum settlements at reduced amounts from individual patients for the same economic reason they accept lower insurance rates: a certain payment now is worth more than an uncertain full payment later.

How much to offer

A reasonable starting offer for a lump-sum settlement is 25 to 50 percent of the remaining balance after insurance, depending on your financial situation and the size of the bill. Start at the lower end of your range to leave room for the billing department to counter while still reaching a settlement that serves your interests. If you have documented financial hardship, a lower initial offer is appropriate. If the bill is large and you can offer a meaningful lump sum, the hospital’s incentive to accept is stronger because the alternative is a payment plan that extends collections over months or years.

The settlement negotiation script

| 🗣 Script: What to Say I am calling to resolve my account number [number]. I have reviewed the itemized bill and I would like to discuss settling this balance. I am not in a position to pay the full amount, but I am prepared to make a lump-sum payment of [$X] today to resolve this account in full. This is the maximum I can pay given my current financial situation. Would you be able to accept this as full settlement of the balance? If they say they need to review with a supervisor: That is absolutely fine. I am available [dates/times]. I want to resolve this as quickly as possible and I am prepared to make the payment as soon as we reach an agreement. If they counter with a higher number: I understand your position. The maximum I can pay as a lump sum is [$Y]. Is there anything you can do to get closer to that number? If they accept: Thank you. Before I process the payment, I need a written settlement agreement confirming that this payment constitutes full and final settlement of this account and that the remaining balance will be written off. Please send that to me at [email or address] before I submit payment. |

Get every agreement in writing before paying

This is not optional. Before you submit any payment under a negotiated settlement, you must have written confirmation from the provider that the agreed amount constitutes full and final settlement of the account and that the remaining balance will be written off rather than sold to a collections agency or pursued further. A verbal agreement over the phone is not sufficient protection. If the billing department sends you only a revised bill rather than a formal settlement letter, ask specifically for written confirmation that the settlement is final and that no further charges will be pursued on this account.

Step 6: Set Up an Interest-Free Payment Plan

If a lump-sum settlement is not financially feasible, a payment plan is your next best option. Most hospitals offer payment plans, and many offer interest-free payment plans to patients who ask. The key is to ask specifically for an interest-free arrangement rather than accepting whatever terms the billing department initially offers.

The payment plan script

| 🗣 Script: What to Say I am not able to pay this balance in full at this time, but I want to make sure it is paid. I would like to set up a payment plan. Does your hospital offer interest-free payment plans for patients? What is the minimum monthly payment you can accept? If they quote a payment above what you can afford: I understand that is your standard minimum, but that amount is more than I can manage given my current income. Could you work with me on a payment of [$X] per month? I want to honor this obligation and I want to make sure the terms are realistic enough that I can actually keep them. |

Most nonprofit hospitals are legally and practically incentivized to work out payment arrangements rather than send accounts to collections, which produces partial recovery at significant cost. A payment plan at any amount prevents the account from going to collections while you make progress on the balance. Do not agree to a payment plan amount that you cannot consistently maintain: missing payments on a payment plan you already set up is worse than negotiating a realistic lower amount from the beginning.

Medical credit cards: what to watch out for

Some billing departments will suggest or actively promote medical credit cards like CareCredit as a payment option. These cards often offer promotional periods with no interest if paid in full within a defined window, typically 12 to 24 months, but charge retroactive interest on the entire original balance at rates of 26 to 29 percent if the balance is not cleared by the end of the promotional period. This is a significant financial risk if you cannot reliably pay off the full balance within the promotional window. An interest-free payment plan directly with the hospital is almost always a better option than a medical credit card if you cannot pay the balance in full.

Step 7: Dispute Bills That Should Have Been Covered by Insurance

Insurance billing errors are as common as provider billing errors, and the consequences of uncorrected insurance errors can be as expensive. The most common insurance billing issues are claims being denied for administrative reasons that can be corrected, services being applied to the deductible that should have been covered before the deductible, and out-of-network charges on services you believed were in-network.

Start with your Explanation of Benefits

Every time your health insurance processes a claim, it sends you an Explanation of Benefits, commonly called an EOB. The EOB is not a bill. It is a record of what was billed to your insurer, what the insurer allowed, what the insurer paid and what you owe as your cost-sharing responsibility. Review every EOB and compare it to the provider’s bill. If the amounts do not match or if a claim is marked as denied, that is the starting point for your insurance dispute.

How to appeal a denied insurance claim

All ACA-compliant health plans are required to have an internal appeals process and to inform you of your right to appeal when a claim is denied. The appeal process has three stages: an internal appeal with your insurer, an expedited appeal for urgent situations and an external review by an independent organization if the internal appeal is unsuccessful.

- Request the specific reason for the denial in writing. The EOB will list a denial reason code but may not explain it clearly. Call your insurer and ask them to explain in plain language why the claim was denied.

- Gather supporting documentation. For a denial based on medical necessity, ask your doctor for a letter supporting the necessity of the treatment. For a denial based on network status, gather documentation that you verified the provider was in-network before your appointment.

- File your written appeal within the insurer’s deadline, which is typically 180 days from the denial date. Include your documentation and a clear explanation of why the denial should be reversed.

- If the internal appeal is denied, request an external review. Under the ACA, you have the right to an independent external review of most coverage denials, and the external reviewer’s decision is binding on the insurer.

The No Surprises Act: your protection against balance billing

The No Surprises Act, which took effect January 1, 2022, prohibits out-of-network providers from balance billing patients for emergency services and for non-emergency services received at in-network facilities without the patient’s advance written consent. If you received an out-of-network bill for care you received at an in-network facility, or for emergency care where you had no choice of provider, review whether the bill violates the No Surprises Act. File a complaint with the Centers for Medicare and Medicaid Services at cms.gov/nosurprises if you believe you have been billed in violation of this law.

Medical Debt in Collections: What You Can and Cannot Do

If a medical bill has already been sent to a collections agency, your options change but do not disappear. Medical debt has specific consumer protections that other types of debt do not have.

The CFPB medical debt credit reporting rule

The Consumer Financial Protection Bureau finalized a rule in 2025 prohibiting the three major credit bureaus from including medical debt on credit reports. This rule, if it survives ongoing legal challenges, would remove medical debt from the credit reporting system entirely, eliminating the credit score damage that has historically driven many Americans to prioritize medical bills over other financial obligations regardless of their financial situation. Check the current status of this rule at cfpb.gov because its implementation status may have changed since this guide was verified in April 2026.

Statute of limitations on medical debt

Medical debt, like all civil debt, has a statute of limitations after which the debt becomes uncollectable through the courts. The statute of limitations for medical debt varies by state, ranging from three to ten years depending on state law and the type of medical agreement involved. After the statute of limitations expires, the collector can no longer successfully sue you to collect the debt. This does not mean the debt disappears or that you are not morally or legally obligated to pay it. It means the collector has lost the most powerful collection tool, the ability to obtain a court judgment and pursue wage garnishment or bank levies.

Negotiating a medical debt in collections

Collections agencies typically purchase medical debt from providers and hospitals at a significant discount, often 10 to 30 cents on the dollar. This means the collection agency has room to negotiate a settlement at a fraction of the original balance while still profiting from the transaction. When negotiating with a medical debt collector, use the same lump-sum settlement approach described in Step 5 and apply the same rule: get any settlement agreement in writing before submitting payment, and confirm that the settlement constitutes full and final resolution of the debt with no further pursuit.

How AI Tools Help You Negotiate Medical Bills

AI tools have become genuinely useful for Americans navigating medical billing disputes in 2026. Here are the specific ways they add value to the process.

Using Claude or ChatGPT to understand your bill

Paste the line items from your itemized bill into Claude at claude.ai or ChatGPT at chatgpt.com and ask for help understanding what each CPT code means, whether the combination of codes billed is typical for the services you received and whether any charges appear inconsistent with standard billing practices for your diagnosis or procedure. AI cannot replace a professional medical billing auditor but can help you quickly understand what you are looking at and identify items worth questioning.

Using AI to draft dispute letters

AI tools generate professional, clear dispute letters based on the specific details of your situation far faster than writing them manually. Provide Claude or ChatGPT with your account number, the specific charges in dispute, the reason you believe they are incorrect and the resolution you are seeking. Ask the AI to draft a formal dispute letter addressed to the billing department and the patient advocate. Review the draft and customize it with your specific details before sending.

Using AI to research your rights

Medical billing law is complex and varies by state. Use Claude or ChatGPT to research the specific consumer protections applicable to your situation: your state’s statute of limitations on medical debt, your rights under the No Surprises Act for your specific situation, the ACA financial assistance requirements applicable to your provider and the specific complaint process for your state’s hospital licensing board. This research takes hours manually and minutes with AI assistance.

| 💡 Pro Tip Use this prompt with Claude or ChatGPT when you receive any medical bill: I received a medical bill from [hospital name] in [state]. My account number is [number]. The total charged is [$amount]. I have the itemized bill in front of me. Help me: 1) understand the most common billing errors to look for in a hospital bill, 2) identify what CPT codes I should look up, 3) draft a request for financial assistance, and 4) write a negotiation script for a lump-sum settlement at approximately 40 percent of the billed amount. I would like to resolve this bill for as little as legally and ethically possible. |

| Strategy | Potential Saving | Time Required | Difficulty | Best When |

| Audit for billing errors | $100 to $5,000+ | 2-4 hours | Medium | Always – do this first |

| Apply for financial assistance | 50-100% of balance | 1-2 weeks | Low | Income qualifies for program |

| Negotiate lump-sum settlement | 20-60% reduction | 1-3 phone calls | Medium | You can pay a lump sum |

| Set up payment plan | Avoids collections | 1 phone call | Low | Cannot pay lump sum |

| Dispute insurance denial | Up to full bill amount | 1-4 weeks | High | Claim was wrongly denied |

| No Surprises Act complaint | Up to full balance | 2-6 weeks | High | Billed for surprise care |

| Negotiate in collections | 30-70% reduction | 1-3 interactions | Medium | Bill already in collections |

| 💡 Real-World Example Consider a hypothetical 38-year-old freelance graphic designer in Austin named Robert who received a $14,700 hospital bill after a two-day admission for a kidney stone. He had an HDHP with a $3,000 deductible and his maximum out-of-pocket was $7,000. Robert’s insurer had already processed the claim and his EOB showed he owed $6,800 after his insurance paid its share. He had met $1,100 of his deductible previously that year, so the remaining $1,900 applied to his deductible, and then 20 percent coinsurance applied to the remaining covered charges. Step 1: Robert requested an itemized bill. He discovered a charge for a consultation with a nephrologist who he did not recall seeing. He called the billing department and asked for documentation of the consultation. The billing department confirmed the nephrologist had reviewed his case remotely but had not physically seen him. This was correctly billed as a telemedicine consultation but Robert verified it was a legitimate service. Step 2: He looked up his hospital’s posted prices under the federal transparency rule and confirmed that the contracted rate with his insurer was applied correctly. Step 3: He called the billing department and asked whether the hospital had a financial assistance program. As a freelancer, his income in the previous tax year was approximately $58,000. The hospital’s financial assistance program covered patients earning up to 300 percent of the federal poverty level, which for a single individual in 2026 was approximately $45,720. Robert’s income was above that threshold. Step 4: He asked whether the hospital had any prompt-pay discounts or hardship discounts for patients above the charity care threshold. The billing representative offered a 20 percent prompt-pay discount if he paid within 30 days. On a $6,800 balance, that reduced the amount to $5,440. Step 5: Robert asked whether they would accept $4,200 as a lump-sum settlement since he had HSA funds from prior years. The representative put him on hold, consulted a supervisor and returned with an offer of $4,800 as a final settlement, which Robert accepted. He received a written settlement letter confirming the $4,800 as full and final resolution. Final outcome: Robert reduced a $6,800 post-insurance balance to $4,800 through a negotiated settlement, saving $2,000 through two phone calls and an hour of research. The entire process took approximately three weeks. This example is illustrative. Actual outcomes depend on individual circumstances, provider policies and state-specific rules. |

Frequently Asked Questions

Is it legal to negotiate medical bills in the US?

Yes, completely. Medical bill negotiation is legal, ethical and widely practiced by every major payer in the US healthcare system including insurance companies, Medicare, Medicaid and self-pay patients. Hospitals and providers accept negotiated rates as a standard business practice. Individual patients negotiating their own bills are doing exactly what every insurer does on behalf of its members.

Will negotiating my medical bill hurt my credit?

Negotiating a bill that is in your name and not yet in collections does not affect your credit score. Only accounts reported to credit bureaus affect your credit, and providers typically do not report accounts to credit bureaus while you are actively communicating and making progress toward payment. The CFPB’s 2025 rule, if its legal challenges are resolved favorably, would further limit medical debt’s ability to affect credit scores. Stay current on any payment arrangements you make to prevent a bill from being sent to collections.

What if the hospital refuses to negotiate?

If the initial billing representative says they cannot negotiate, ask to speak with a patient advocate, a patient financial counselor or a billing supervisor. These roles have more authority to approve exceptions than frontline billing staff. If the hospital still refuses to engage, contact your state’s hospital licensing board or the American Hospital Association’s patient advocacy resources. Nonprofit hospitals that refuse to provide information about their financial assistance programs may be violating their obligations under the ACA.

How long do I have to dispute a medical bill?

There is no federal time limit on disputing a medical bill before it goes to collections, but acting quickly is always in your interest. Most providers send accounts to collections after 60 to 180 days of nonpayment depending on their internal policies. For insurance appeals, ACA-compliant plans allow 180 days from the date of denial to file an internal appeal. For external reviews, the deadline varies but is typically 60 days after the internal appeal decision.

Can a hospital sue me for an unpaid medical bill?

Yes, hospitals can pursue legal action for unpaid medical bills and can obtain court judgments that allow wage garnishment in states where medical debt wage garnishment is permitted. However, nonprofit hospitals are prohibited from pursuing legal action against patients who qualify for financial assistance before making a reasonable effort to determine whether they qualify. If you receive a lawsuit notice from a hospital, respond immediately by contacting a local legal aid organization or patient advocate rather than ignoring the notice, which would result in a default judgment.

- Patient Advocate Foundation: nonprofit providing case management services and financial aid to Americans with serious illness facing billing challenges. Opens in new tab.

- CFPB Medical Billing Resources: free resources on your rights regarding medical debt and billing. Opens in new tab.

- CMS No Surprises Act Patient Resources: official information and complaint filing for violations of the federal No Surprises Act. Opens in new tab.

- FAIR Health Consumer: free tool to look up typical charges and allowed amounts for medical procedures in your area. Opens in new tab.

- Healthcare Bluebook: free fair market price comparisons for hundreds of medical procedures by location. Opens in new tab.

| ⭐ Key Takeaway Receiving a medical bill is not the end of a financial process. It is the beginning of a negotiation. The itemized bill, the price transparency data, the financial assistance application and the lump-sum settlement offer are four tools that most Americans never use because no one tells them these options exist. Now you know they exist. The next time you receive a medical bill, do not pay it immediately. Request the itemized version, audit it, look up the price data, ask about financial assistance and then negotiate from an informed position. The hospital billing department is used to these conversations. They have the authority to reduce bills, accept settlements and set up interest-free payment plans. What they do not have is any obligation to offer these options unless you ask specifically for them. |

Conclusion

Medical bills are negotiable. Billing errors are common. Financial assistance exists at every nonprofit hospital in the country. Lump-sum settlements at significantly reduced amounts are accepted every day. Insurance denials can be appealed. Surprise bills can be disputed under federal law. Most Americans pay more than they are required to pay because they do not know these tools exist or do not know how to use them.

This guide has given you every tool and every word you need to reduce any medical bill you receive in the United States. The process is not quick and it is not always comfortable, but a few phone calls using the scripts in this guide regularly produce savings of 20 to 60 percent on medical bills that Americans would otherwise pay in full without question.

For Americans planning how to manage healthcare costs as part of their long-term financial strategy, our guide on how to choose the right health insurance plan during open enrollment covers how to select a plan that minimizes your total healthcare costs before bills arrive. For those building the financial foundation that makes medical cost surprises manageable, our guide on best high yield savings accounts in the US 2026 covers where to keep your emergency fund earning the highest available rate.

| 📥 Free Download: Medical Bill Negotiation Script Pack 2026 Word-for-word phone scripts, dispute letter templates and a medical bill audit checklist for negotiating and correcting medical bills in the US Free. Email required. For informational purposes only. Not legal or medical advice. |

| 📲 Share This Guide If this guide helped you understand that your medical bill is negotiable and gave you the words to do something about it, share it with someone who received a bill they cannot afford. Share on WhatsApp, Facebook or by text message. Thank you for reading TechAIFinance.com. |

Read Next

Continue building your financial knowledge on TechAIFinance.com:

- How to Choose the Right Health Insurance Plan During Open Enrollment

- Best High Yield Savings Accounts in the US 2026

- How to Build Generational Wealth in the US

- How to Retire Early Using the FIRE Method in the US 2026

- Best Ways to Make Money During a Recession in the US

| ✍ About the Author Written by: TechAIFinance Editorial Team Edited and Fact-Checked by: Olayinka Adejugbe Olayinka Adejugbe is not a licensed financial advisor. The content on TechAIFinance.com is produced for educational purposes only and should not be treated as personalized financial advice. Olayinka is the founder and lead editor of TechAIFinance.com. He holds a Global Certification in Artificial Intelligence and Applied Innovation and an Award of Completion in Behavioral Counseling from the World Health Organization. With a strong working knowledge of personal finance and accounting principles, Olayinka oversees the editorial review of every article on this site to ensure accuracy, currency and practical usefulness. Every article on TechAIFinance.com is produced by our research team and reviewed by Olayinka before publication. We verify statistics against named authoritative sources and update content when circumstances change. Visit our About page to learn more about our editorial process. Use our Contact page to get in touch. |

Important Disclaimer

The content published on TechAIFinance.com is for educational and informational purposes only. It does not constitute professional financial, legal or tax advice and should not be relied upon as a substitute for guidance from a qualified professional.

Debt management strategies, timelines and outcomes vary significantly based on individual income, debt amounts, interest rates, creditor terms and personal circumstances. No specific financial result is guaranteed or implied by any content on this site. Always consult a qualified financial advisor, credit counselor or attorney before making significant financial decisions. Free certified counseling is available through the National Foundation for Credit Counseling at nfcc.org.